Global Premium Liqueur Market – Industry Trends and Forecast to 2030

Report ID: MS-800 | Food and Beverages | Last updated: Apr, 2025 | Formats*:

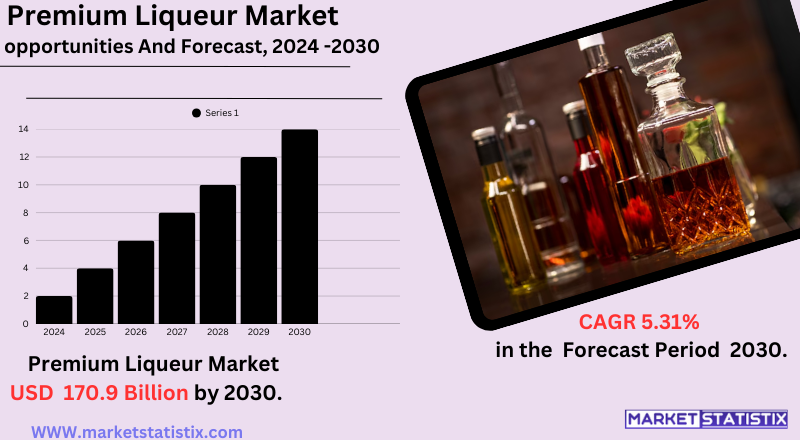

Premium Liqueur Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 5.31% |

| Forecast Value (2030) | USD 170.9 Billion |

| By Product Type | Coffee Liqueur, Nuts Liqueur, Fruit Liqueur, Chocolate Liqueur, Other |

| Key Market Players |

|

| By Region |

|

Premium Liqueur Market Trends

The premium liqueur market is currently undergoing some remarkable trends. One of the strongest driving phenomena is premiumisation as a consumer trend, which means consumers are beginning to choose quality and uniqueness when it comes to liqueurs instead of standard offerings. This trend is further fuelled by the craftsmanship of the liqueurs and their ingredients and flavouring nuances. The consumers would go all out and spend for an experience that is thought to be elevated – whether it is sipping liqueur neat, making the classic cocktails, or experimenting with new concoctions at home. One of the other major trends is the recent rise in popularity of cocktail culture and setting up home bars. Premium liqueurs provide excellent ingredients with flavours profiled and complexities to create a top-shelf cocktail. Demand for these categories continues to grow, inspiring bartenders and mixologists at home to look for unique liqueurs and artisanal options. Flavours have also been a big draw, as producers experiment with strange and exotic ingredients and lower-sugar and natural ingredients geared toward health-conscious consumers.Premium Liqueur Market Leading Players

The key players profiled in the report are Marie Brizard Wine & Spirits (France), William Grant & Sons Ltd. (Scotland), Pernod Ricard (France), Remy Cointreau (France), Diageo plc (United Kingdom), Beam Suntory Inc. (United States), Brown-Forman Corporation (United States), Campari Group (Italy), The Edrington Group (Scotland)Growth Accelerators

The premium liqueur market is currently booming with a growth spurt, with various major drivers holding it up. First among these would be the rise of disposable income in developing economies, which allows a larger consuming population to, in fact, afford and indulge in high-priced alcoholic beverages of the premium range. This scenario is coupled with the growing consumer sentiment towards quality and authenticity, with customers seeking unique flavours, superlative ingredients, and artisanal production tools rather than those in mass production. This premiumisation trend is visible in other consumer goods, and liqueurs have not been spared either. Of equal importance have been the cocktail culture and home-cocktailing. Premium liqueurs form the backbone of truly sophisticated and flavourful cocktails both in restaurants and homes. Social media and online tutorials have thereby helped nurture the trend of experimentation and an interest in utilising only the highest quality liqueurs for desired taste profiles.Premium Liqueur Market Segmentation analysis

The Global Premium Liqueur is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Coffee Liqueur, Nuts Liqueur, Fruit Liqueur, Chocolate Liqueur, Other . The Application segment categorizes the market based on its usage such as Restaurants, Bar/Pubs, Others. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

Premium liqueur markets are more gifted with international players, but they also have a large array of budding artisanal producers. A good number of international beverage companies include premium liqueur brands in their larger portfolios of spirits and leverage wide distribution and high recognition. Such players compete based on heritage, quality, and availability. At the same time, a vibrant craft and speciality liqueur player is very much focused on flavours – their products are composed from natural ingredients and are produced in a small-scale operation and are often in the hands of some, but fewer, consumers who want a more individualistic experience. Besides that, cocktail culture and home bartenders have opened doors for brands to showcase a wideness of their premium liqueurs in both classic and innovative cocktails, hence increasing competition and development of the products within the market.Challenges In Premium Liqueur Market

The premium liqueur landscape is beset with challenges such as regulatory complexities and supply chain frailties. Different tax structures that have to be dealt with tight alcohol regulations in different areas hold back production, distribution, and compliance, leading to an increase in overall operational costs. There are climate-related disruptions that cause crop shortages and create bottlenecks in logistics and jeopardise future availability and price stability of raw materials – more so natural and organic sources. Similarly, high-sugar liqueurs will feel the heat from a health-hungry crowd, while luxury drinks spending will likely suffer due to economic vulnerabilities. There are further issues from competition and consumer behaviour changes. Established brands dominate in terms of distribution and heritage such that craft producers find it increasingly difficult to enter the market. So rapid is the change in consumer preference for RTDs and exotic flavours that keeping up with demands requires constant innovative thinking and investment in research and development. Counterfeits have indeed undermined the trust accorded to brands, even as local players use local flavours and marketing to fragment the market further. These conditions will thus call for agile strategies balancing premiumisation against accessibility and sustainability.Risks & Prospects in Premium Liqueur Market

The rise of increasingly unique and artisanal products now applies to flavours such as orange, cherry, and melon that were formerly considered relatively novel in tequila-based cocktails. The increasing social acceptance of alcohol in the emerging markets of the world, along with the growth in bars, hotels and e-commerce, would most certainly increase accessibility and consumption in the Asia-Pacific and Latin America regions. Regionally, Europe being the leading region in terms of the consumption patterns associated with premium products, North America benefits from high throwaway incomes and strong distribution networks. Fast growth in the Asia Pacific has brought about the advancement of urbanisation, growing middle populations, and Westernisation of drinking habits, such as in China and India. For example, Latin America would be further enhanced with increasing capital investments in hospitality businesses towards the encouraging adoption of cocktail culture, while mature markets would switch off to premiumisation and diversification in flavours for continuous growth.Key Target Audience

The premium liqueurs basically target the affluent Millennials and the Gen Z consumers. They idealise quality and craftsmanship and go for taste that is unique. They have a penchant for these craft and artisanal liqueurs, as they offer authenticity and some newer aspects of taste, such as the infusion of botanicals and exotic fruits. The cocktail culture and the mixing at home also create a need for versatile liqueurs that are suitable for cocktails, which consumers will enjoy actually doing at home.,, Hipro commercial establishments, i.e., high-end bars, restaurants, and hotels, are another big audience of whom premium liqueurs are used as a cocktail ingredient to give cocktails uniqueness to the establishment and bring in upscale clientele. Culture of gifting: Premium liqueurs are important because they are associated with luxury, and their packaging makes them better suited for gifting on special occasions and even for corporate gifting. Emerging markets are gradually becoming part of the potential market for premium liqueurs as disposable incomes grow and access to the international drinking culture enhances global drinking trends. Brands will see more and more growth opportunities for those that will position themselves as unique in product differentiation and experiences.Merger and acquisition

Over the years, this market for high-quality liqueurs went through many mergers and acquisition activities. These were efforts made towards expanding portfolios and reaching markets by major spirits companies. In 2024, Campari Group completed the largest acquisition in its history by purchasing French cognac producer Courvoisier for a sum that is estimated at about €1.22 billion. This was intended to bolster its presence in premium cognac and enhance its footprint in key markets such as the US and China. Although this is ongoing despite the challenges, like that of China's anti-dumping investigation on EU brandy, Campari plans to drive growth through leveraging Courvoisier's market position. Another important activity was Bacardi acquiring Ilegal Mezcal, the super-premium mezcal brand, in 2023 to add to its high-end spirits portfolio. Also, Sazerac Company bought ready-to-drink cocktail brand BuzzBallz in March 2024 and took over Svedka vodka from Constellation Brands in January 2025. Such acquisitions go hand in hand with what seems to be a larger industry trend in which top spirits companies move to acquire or develop high-domain and innovation brands in an attempt to satisfy evolving consumer preferences and consolidate competitive positions. >Analyst Comment

The premium liqueur market is steadily growing due to increasing demand for quality flavoured alcoholic drinks and consumers' shifting preferences towards premiumisation of spirits. Although exact data regarding premium liqueurs are not specifically reported, the liqueur industry is forecast to grow from $131.3 billion in 2024 to approximately $164 billion in 2033, with premiumisation likely to outrun this figure on account of trends such as exotic flavour innovations and cocktail culture. The global premium alcoholic beverages market – a classification that encompasses liqueurs – is expected to soar from $596.8 billion in 2025 to $950.8 billion by the year 2030, an increase that would mirror consumer willingness to spend on luxury products.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Premium Liqueur- Snapshot

- 2.2 Premium Liqueur- Segment Snapshot

- 2.3 Premium Liqueur- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Premium Liqueur Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Coffee Liqueur

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Nuts Liqueur

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Chocolate Liqueur

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Fruit Liqueur

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

- 4.6 Other

- 4.6.1 Key market trends, factors driving growth, and opportunities

- 4.6.2 Market size and forecast, by region

- 4.6.3 Market share analysis by country

5: Premium Liqueur Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Bar/Pubs

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Restaurants

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Others

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Premium Liqueur Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Pernod Ricard (France)

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Remy Cointreau (France)

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Marie Brizard Wine & Spirits (France)

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Diageo plc (United Kingdom)

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Brown-Forman Corporation (United States)

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Beam Suntory Inc. (United States)

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Campari Group (Italy)

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 William Grant & Sons Ltd. (Scotland)

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 The Edrington Group (Scotland)

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the estimated market size of Premium Liqueur in 2030?

+

-

Which type of Premium Liqueur is widely popular?

+

-

What is the growth rate of Premium Liqueur Market?

+

-

What are the latest trends influencing the Premium Liqueur Market?

+

-

Who are the key players in the Premium Liqueur Market?

+

-

How is the Premium Liqueur } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Premium Liqueur Market Study?

+

-

What geographic breakdown is available in Global Premium Liqueur Market Study?

+

-

How are the key players in the Premium Liqueur market targeting growth in the future?

+

-

What are the opportunities for new entrants in the Premium Liqueur market?

+

-