North America Catering and Food Service Contractor Market Size, Share & Trends Analysis Report, Forecast Period, 2024-2030

Report ID: MS-847 | Healthcare and Pharma | Last updated: May, 2025 | Formats*:

The Catering and Food Service Contractor Market involves businesses that offer food and beverage service outsourcing to varied clients and establishments. These contractors handle all or part of food preparation, distribution, and presentation, sometimes taking place within the client's buildings or from a central kitchen base. Their capabilities go beyond culinary preparation to cater to menu preparation, ingredient buying, kitchen coordination, staff arrangements, and food safety compliance. This market addresses organizations that are willing to outsource their food service operations to professional external parties instead of having them operate internally.

The coverage of the Catering and Food Service Contractor Market is extensive, covering sectors including corporate offices, educational facilities (schools and universities), medical centers (hospitals and nursing homes), government offices, industrial campuses, and event sites. These contractors provide tailored solutions based on the individual needs and size of each customer, from daily meal provision to staff or students to catering for large events. It is driven by market drivers such as growing organisational interest in focusing on core competencies, cost savings from outsourcing, and the need for variety and quality of food.

Catering and Food Service Contractor Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

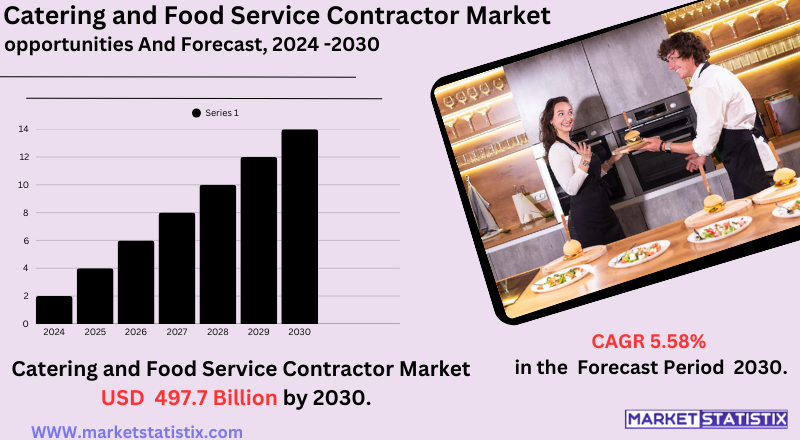

| Growth Rate | CAGR of 5.58% |

| Forecast Value (2030) | USD 497.7 Billion |

| By Product Type | Food Service Contractors, Caterers |

| Key Market Players | Compass Group Plc. (United Kingdom), Sodexo (France), Aramark Corporation (United States), Elior Group (France), Delaware North (United States), Westbury Street Holdings (United States), Ovations Food Services (United States), Thompson Hospitality (United States), Dine Contract Catering (United Kingdom) , Olive Catering Services (United Kingdom) |

| By Region |

|

Catering and Food Service Contractor Market Trends

The major driver is the rising trend for food services to be outsourced by institutions such as corporations, hospitals, and schools so that they can devote themselves to core operations while experts manage food. It is further spurred by demand for personalised and convenient meal solutions such as meals designed for eating preferences like vegetarian, vegan, and gluten-free. Increased consciousness and focus on health and well-being are also compelling contractors to provide healthier and better-balanced meal alternatives, using fresh and organic ingredients.

Another trend of significance is the increasing use of technology throughout the industry. These involve online ordering websites, customer mobile apps, meal planning by AI, and food preparation robots, all directed towards enhancing efficiency, customer satisfaction, and operation smoothness. In addition, there is also a discernible surge in demand for catering facilities for different functions, from corporate events and weddings to smaller social gatherings, echoing a larger pattern of convenience and the need for professionally run food and beverage arrangements. These tendencies all point toward a dynamic and changing market accommodating shifting consumer trends and technological advancements.

Catering and Food Service Contractor Market Leading Players

The key players profiled in the report are Compass Group Plc. (United Kingdom), Sodexo (France), Aramark Corporation (United States), Elior Group (France), Delaware North (United States), Westbury Street Holdings (United States), Ovations Food Services (United States), Thompson Hospitality (United States), Dine Contract Catering (United Kingdom), Olive Catering Services (United Kingdom)Growth Accelerators

The Catering and Food Service Contractor Market is driven by a number of major drivers that mirror changing economic and societal environments. To begin with, the growing practice of outsourcing non-core functions by companies and institutions continues to be a major driver. Organizations in different sectors, such as corporate, education, and healthcare, are discovering it more efficient and cost-effective to outsource their food service functions to professional contractors so that they can concentrate on their core goals. This trend for outsourcing gives the contractor a regular demand for its services.

Secondly, convenience and the increasing lifestyles of working people play a major role in market expansion. With increasingly hectic schedules and higher demands for readily available meal options, more organizations and individuals rely on catering and food service contractors for daily meals, events, and special events. In addition, increasing demand for healthier and more varied food, such as tailored menus to meet particular dietary requirements and tastes, is compelling contractors to innovate and extend their services, further driving market growth.

Catering and Food Service Contractor Market Segmentation analysis

The North America Catering and Food Service Contractor is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Food Service Contractors, Caterers . The Application segment categorizes the market based on its usage such as Educational Institutions, Industrial, Healthcare, Hospitality Services, Sports & Leisure, Corporate, Other. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The Catering and Food Service Contractor Competitive Landscape Analysis indicates a vibrant and increasingly competitive marketplace. The industry consists of a combination of large, global companies with deep resources and diverse service offerings and many smaller, regional, or niche companies serving specialised industries or cuisine categories. Competition is fierce on multiple dimensions such as pricing, service, menu creativity, technological adoption (such as online ordering and catering management software), and the capacity to service different dietary requirements and preferences such as sustainable and healthy choices.

Major competitive strategies focus on establishing strong client relationships, providing customized and flexible service solutions, and showcasing efficiency and reliability in operations. Differentiation is attained through distinct culinary offerings, orientation towards particular market segments (corporate, healthcare, education), and the implementation of technology for process efficiency and customer satisfaction.

Challenges In Catering and Food Service Contractor Market

The catering and food services contractor market is also confronted with some major challenges that affect growth and operational effectiveness. Volatile raw material and food costs, endemic supply chain interruptions, and increasing labour costs exert pressure on already thin profit margins, and cost control is an ongoing challenge for operators. The industry also has to deal with rigorous and dynamic food safety legislation, which raises the costs of compliance and necessitates regular staff training and operational modifications. Staff shortages and high staff turnover also put additional pressure on service quality and consistency, particularly as the industry has difficulty recruiting and maintaining qualified staff.

Fierce competition – both from big multinational companies and smaller, niche caterers – increases the challenge, compelling firms to differentiate through innovation, technology adoption, and sustainability efforts. Economic and geopolitical volatilities, including tariff fluctuations and regulatory changes, introduce additional uncertainty in planning and investment. To stay competitive, market participants need to be agile, collaborate along the value chain, and customise strategies to local conditions while ensuring compliance and operational resilience.

Risks & Prospects in Catering and Food Service Contractor Market

Key opportunities in the market involve increased demand for affordable, high-quality, and convenient food services and technology adoption, such as online ordering and food management software. The trends toward healthier and more sustainable menu choices are also being exploited by companies, with the major players investing in R&D and widening their service offerings to appeal to new segments in the market.

Regionally, North America and Europe are leading the market now with established infrastructure, high disposable incomes, and the strong presence of top contractors. Nevertheless, the Asia-Pacific region is expected to grow at the fastest rate, driven by urbanisation, increasing disposable incomes, and changing consumer behaviour. Emerging markets in Africa and the Middle East also have huge potential as organizations outsource food services more and more to enhance efficiency and concentrate on core activities.

Key Target Audience

The primary target clientele for the food service and catering contractor market consists of institutions like schools, hospitals, military facilities, and corporate buildings that contract out their food service activities. These customers focus on cost savings, quality consistency, and adherence to health and safety standards. They tend to look for long-term relationships with contractors who are capable of providing tailored meal options, mass production of food, and support for special diets while ensuring operational efficiency.Another major audience category consists of wedding coordinators, event planners, and private clients for catering special events. This segment holds value for flexibility, presentation quality, menu diversity, and punctuality. Due to the increasing focus on sustainability and healthy eating, most clients also demand contractors provide organic, locally grown, and environmentally friendly food options. Such demands compel contractors to be creative in designing menus and delivering services to keep pace with a diverse and dynamic market.

,,

Merger and acquisition

The catering and food service contractor market has seen significant merger and acquisition (M&A) activity in recent years due to strategic growth and consolidation drives. For example, Compass Group, the global leader in catering, has been aggressively acquiring companies to enhance its European presence. Some of its recent acquisitions are Norway's 4Service for $500 million and France's Dupont Restauration for $300 million. These steps are a part of Compass's plan to take advantage of robust outsourcing demand and duplicate its successful North American model in Europe.

Meanwhile, French catering company Sodexo has been weighing a major acquisition of U.S. rival Aramark, a deal worth potentially about $10 billion. But the possible merger has been a cause of concern among investors because of its heavy debt burden and the difficulty of merging two huge companies in a low-margin sector. Apart from this, the move is part of an industry-wide trend where business houses are trying to get wider global reach and enjoy economies of scale through strategic acquisition.

>Analyst Comment

The international catering and food service contractor industry is witnessing strong growth, with market estimates varying from around USD 295 billion in 2024 to around USD 430–470 billion by the year 2030. This growth is driven by increasing demand for outsourced catering within organizations and institutions, increasing urbanisation, and more social and corporate events demanding professional catering services. The industry is also being helped by the use of more advanced technologies like artificial intelligence and smart kitchen systems, which are streamlining operational efficiency, menu personalisation, and food safety standards.

- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Catering and Food Service Contractor- Snapshot

- 2.2 Catering and Food Service Contractor- Segment Snapshot

- 2.3 Catering and Food Service Contractor- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Catering and Food Service Contractor Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Food Service Contractors

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Caterers

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Catering and Food Service Contractor Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Corporate

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Industrial

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Hospitality Services

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Healthcare

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

- 5.6 Educational Institutions

- 5.6.1 Key market trends, factors driving growth, and opportunities

- 5.6.2 Market size and forecast, by region

- 5.6.3 Market share analysis by country

- 5.7 Sports & Leisure

- 5.7.1 Key market trends, factors driving growth, and opportunities

- 5.7.2 Market size and forecast, by region

- 5.7.3 Market share analysis by country

- 5.8 Other

- 5.8.1 Key market trends, factors driving growth, and opportunities

- 5.8.2 Market size and forecast, by region

- 5.8.3 Market share analysis by country

6: Catering and Food Service Contractor Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Compass Group Plc. (United Kingdom)

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Sodexo (France)

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Aramark Corporation (United States)

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Elior Group (France)

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Delaware North (United States)

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Westbury Street Holdings (United States)

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Ovations Food Services (United States)

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Thompson Hospitality (United States)

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Dine Contract Catering (United Kingdom)

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Olive Catering Services (United Kingdom)

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Catering and Food Service Contractor in 2030?

+

-

Which application type is expected to remain the largest segment in the North America Catering and Food Service Contractor market?

+

-

How big is the North America Catering and Food Service Contractor market?

+

-

How do regulatory policies impact the Catering and Food Service Contractor Market?

+

-

What major players in Catering and Food Service Contractor Market?

+

-

What applications are categorized in the Catering and Food Service Contractor market study?

+

-

Which product types are examined in the Catering and Food Service Contractor Market Study?

+

-

Which regions are expected to show the fastest growth in the Catering and Food Service Contractor market?

+

-

Which application holds the second-highest market share in the Catering and Food Service Contractor market?

+

-

What are the major growth drivers in the Catering and Food Service Contractor market?

+

-

The Catering and Food Service Contractor Market is driven by a number of major drivers that mirror changing economic and societal environments. To begin with, the growing practice of outsourcing non-core functions by companies and institutions continues to be a major driver. Organizations in different sectors, such as corporate, education, and healthcare, are discovering it more efficient and cost-effective to outsource their food service functions to professional contractors so that they can concentrate on their core goals. This trend for outsourcing gives the contractor a regular demand for its services.

Secondly, convenience and the increasing lifestyles of working people play a major role in market expansion. With increasingly hectic schedules and higher demands for readily available meal options, more organizations and individuals rely on catering and food service contractors for daily meals, events, and special events. In addition, increasing demand for healthier and more varied food, such as tailored menus to meet particular dietary requirements and tastes, is compelling contractors to innovate and extend their services, further driving market growth.