North America Brain Ischemia Market – Industry Trends and Forecast to 2030

Report ID: MS-854 | Healthcare and Pharma | Last updated: May, 2025 | Formats*:

The brain ischaemia market refers to the economic processes of diagnosis, management, and treatment of an illness where there is inadequate blood supply to the brain. This lower blood flow results in a lack of oxygen and nutrients, which can result in brain tissue damage and lead to numerous neurological disorders such as stroke and vascular dementia. The market comprises pharmaceuticals used for preventing blood clots and risk factor management, medical devices for use in diagnostic tests and interventions such as thrombectomy and angioplasty, rehabilitation services, and assistive devices for patients recovering from ischaemic attacks. The growing incidence of cerebrovascular diseases, together with the ageing population worldwide and increased awareness of risk factors such as diabetes and hypertension, are strong drivers for this market.

Brain Ischemia Report Highlights

| Report Metrics | Details |

|---|---|

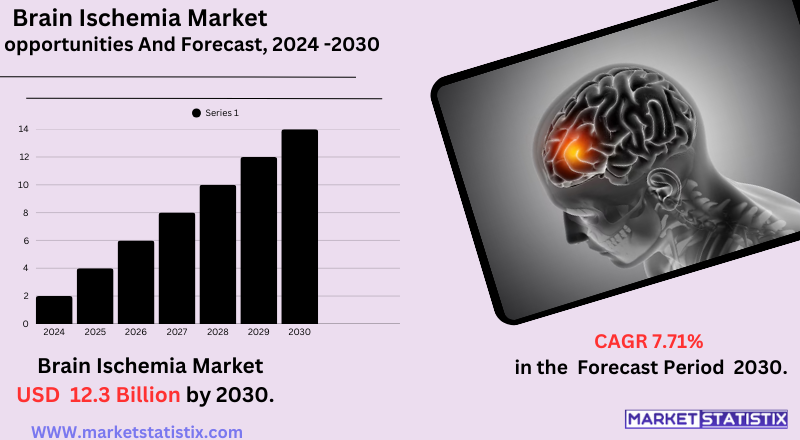

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 7.71% |

| Forecast Value (2030) | USD 12.3 Billion |

| By Product Type | Focal Brain Ischemia, Global Brain Ischemia |

| Key Market Players | Abbott (United States) AstraZeneca (United Kingdom) Bayer AG (Germany) Boehringer Ingelheim International GmbH(Germany) Boston Scientific Corporation (United StatesBristolMyers Squibb Company (United States) Cook (United Kingdom) Edwards Lifesciences Corporation (United States) H. Lundbeck A/S (United States) Johnson & Johnson Private Limited (United India) Merck KGaA (Germany) Novartis AG (Switzerland) Oxurion NV (Belgium) Taxus Cardium Pharmaceuticals Group (CRXM)(United States) Vernalis (R&D) Limited (United Kingdom) Others |

| By Region |

|

Brain Ischemia Market Trends

The ageing population worldwide is one of the primary drivers, with the prevalence of brain ischaemia, including stroke, rising with age. The demographic trend translates into a bigger pool of patients at risk for the condition, thereby driving up demand for diagnostic, therapeutic, and rehabilitative services and products. Additionally, the increased prevalence of concomitant risk factors like hypertension, diabetes, obesity, and cardiovascular diseases fuels the increasing size of the market. These conditions of lifestyle are increasingly common globally, thereby raising the probability of ischaemic events.

Another well-known trend is the relentless evolution in treatment and medical technology. These advances encompass more powerful thrombolytic agents (clot-busting medication) with greater therapeutic windows and lesser side effects and new mechanical thrombectomy devices for actual removal of the blood clot. Progress in imaging modalities such as MRI and CT scans also enhances the pace and accuracy of diagnosis, making possible early intervention.

Brain Ischemia Market Leading Players

The key players profiled in the report are Novartis AG (Switzerland), Merck KGaA (Germany), H. Lundbeck A/S (United States), Vernalis (R&D) Limited (United Kingdom), AstraZeneca (United Kingdom), Boston Scientific Corporation (United StatesBristolMyers Squibb Company (United States), Oxurion NV (Belgium), Johnson & Johnson Private Limited (United India), Cook (United Kingdom), Bayer AG (Germany), Edwards Lifesciences Corporation (United States), Taxus Cardium Pharmaceuticals Group (CRXM)(United States), Abbott (United States), Boehringer Ingelheim International GmbH(Germany), OthersGrowth Accelerators

The market for brain ischaemia is greatly impacted by a number of important drivers that drive its growth and development. First, the rising incidence of cerebrovascular diseases, including stroke and transient ischaemic attacks (TIAs), is a key driver. As these conditions become increasingly prevalent as a result of lifestyle, diet, and physical inactivity, demand for effective diagnostic and therapeutic strategies for brain ischaemia increases proportionally. This increasing pool of patients requires sophisticated medical treatments both for acute conditions and long-term care.

Secondly, an ageing global population is an equally important factor. Older adults have a higher tendency to contract cerebrovascular disease, hence a major target audience for the brain ischaemia market. With this is added growing awareness about brain ischaemia's risk factors of hypertension, diabetes, hyperlipidaemia, and smoking. Growing public health efforts and educational campaigns are causing earlier diagnosis and active management of such risk factors, further propelling the demand for associated healthcare products and services.

Brain Ischemia Market Segmentation analysis

The North America Brain Ischemia is segmented by Type, and Region. By Type, the market is divided into Distributed Focal Brain Ischemia, Global Brain Ischemia . Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The competitive dynamics in the brain ischaemia market are marked by the intense interaction among traditional pharmaceutical and medical device behemoths and a rising cluster of innovative biotech and digital health firms. The large pharma players typically engage in formulating and commercialising thrombolytic agents, antiplatelets, anticoagulants, and neuroprotectants intended to forestall and treat ischaemic incidents. At the same time, mass medical device giants control the market for interventional procedures, marketing sophisticated neuroimaging devices and tools for mechanical thrombectomy and angioplasty. Well-established players gain from wide-reaching distribution networks, robust brand positioning, and impressive research and development resources.

On the other hand, the market is also being confronted with a growing challenge from smaller, but nimbler, biotech companies and startups. These firms tend to focus on new therapeutic modalities, including regenerative therapies, cell-based therapies, and new drug delivery systems. In addition, the rise of digital health firms using artificial intelligence for enhanced diagnostics and treatment planning is introducing an additional level of competition. Collaborations, licensing deals, and acquisitions are prevalent tactics as larger firms look to integrate innovative technologies and broaden their portfolios, while smaller firms look to access markets and capital.

Challenges In Brain Ischemia Market

The market for brain ischaemia is beset by various key challenges that restrict its development even with mounting demand and constant innovation. Treatment is expensive and stands as the key obstacle, especially for novel treatments, surgeries, and extensive rehabilitation. This expense renders it unaffordable to most patients, particularly those from low- and middle-income areas, so treatment is often delayed or even foregone and ultimately results in worse health. Moreover, the lengthy and strict regulatory approval procedures for new medicines and medical devices delay market entry and raise development costs, further constraining the supply of innovative solutions.

Another serious challenge is low awareness and early detection of brain ischaemia symptoms among the general population and even among healthcare providers, which too often leads to delayed diagnosis and treatment. This problem is compounded in settings with poor healthcare infrastructure, where there is limited access to high-quality diagnostic equipment and specialised services. In addition, the heterogeneity of the patient response to therapy and the complexity of the disorder makes it challenging to formulate uniform protocols, and consistent and effective care across different populations proves elusive.

Risks & Prospects in Brain Ischemia Market

Major areas of development are new neuroprotective agents, the use of sophisticated imaging and artificial intelligence for early detection, and the broadening of minimally invasive surgery. Research and development investments are being made by pharmaceutical and medical device companies to leverage the increasing demand for effective treatments and the increased awareness of stroke prevention and treatment.

Regionally, the market is dominated by North America and Europe as a result of their well-established healthcare infrastructures, greater brain ischaemia prevalence, and substantial presence of top industry players. The Asia-Pacific region, most notably China, India, and Japan, will experience the greatest growth, driven by accelerating economic growth, expanding healthcare expenditure, and a significant, underserved patient population. These forces create financially rewarding prospects for market participants as emerging markets pour money into health care infrastructure and awareness initiatives and further extend health care access to innovative drugs and diagnostics.

Key Target Audience

The most important target group in the brain ischaemia market consists of healthcare professionals like neurologists, neurosurgeons, emergency doctors, and hospital administrators who are directly responsible for diagnosing and treating stroke and ischaemic brain disorders. These professionals depend on cutting-edge diagnostic devices, efficient drugs with therapeutic potential, and the latest surgical techniques to enhance patient outcomes. Druggists and med device companies reformulate and develop their products, as well as their promotional packages, to serve the clinical needs of these individuals, highlighting efficiency, quickness of effect, and safety profiles.

,, The other key audiences are research organizations, academic medical centers, and biotechnology companies involved in neuroscience and cerebrovascular research. Such stakeholders are focused on novel treatments, biomarkers, and clinical trial results underpinning new treatment development. Policymakers, payers, and insurers are a second audience, whose interests drive market access, reimbursement, and regulation—important drivers of the commercial success of brain ischaemia-related offerings and services.

,

Merger and acquisition

Recent acquisitions and mergers in the brain ischaemia space indicate a strategic move by large healthcare and pharmaceutical firms to increase their portfolios and improve treatment options. In August 2024, Johnson & Johnson announced that it had acquired V-Wave Ltd., a firm working on new treatment solutions for heart failure, for an initial payment of $600 million, with possible additional payments of up to $1.1 billion. This acquisition will help strengthen Johnson & Johnson's MedTech business and may have an impact on cerebrovascular treatment options. In June 2024, Boston Scientific Corporation also signed a definitive agreement to acquire Silk Road Medical, Inc., a company that develops minimally invasive solutions to prevent stroke in patients suffering from carotid artery disease, for about $1.16 billion. Among significant developments in the Asia-Pacific market is the September 2023 licensing deal between Sun Pharmaceutical Industries and Pharmazz to market Tyvalzi (Sovateltide) in India.

This collaboration seeks to bring a new treatment for cerebral ischaemic stroke to market, increasing access to cutting-edge treatments in emerging economies. Furthermore, the merger of Cycle Pharmaceuticals and Vanda Pharmaceuticals in June 2024, worth $466 million, represents a consolidation trend aimed at strengthening therapeutic options in neurology. The acquisitions and alliances represent the highly dynamic nature of the brain ischaemia market based on the urgency for sophisticated treatment and the exploration of new geographies.

>

Analyst Comment

The brain ischaemia market globally is expanding significantly, and market valuations are expected to increase from about USD 780–850 million during 2022–2024 to about USD 1.5 and 1.6 billion in 2031–2032. The reason for this growth is mainly attributed to the expanding incidence of cerebrovascular disease like stroke and transient ischaemic attack, increased geriatric populations, and better awareness of the symptoms and danger of brain ischaemia among clinicians and patients. Technological advancements in diagnostic imaging, such as MRI and CT scans, have provided earlier and precise detection, further aiding the growth of the market.

- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Brain Ischemia- Snapshot

- 2.2 Brain Ischemia- Segment Snapshot

- 2.3 Brain Ischemia- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Brain Ischemia Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Focal Brain Ischemia

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Global Brain Ischemia

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Brain Ischemia Market by Region

- 5.1 Overview

- 5.1.1 Market size and forecast By Region

- 5.2 North America

- 5.2.1 Key trends and opportunities

- 5.2.2 Market size and forecast, by Type

- 5.2.3 Market size and forecast, by Application

- 5.2.4 Market size and forecast, by country

- 5.2.4.1 United States

- 5.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 5.2.4.1.2 Market size and forecast, by Type

- 5.2.4.1.3 Market size and forecast, by Application

- 5.2.4.2 Canada

- 5.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.4.2.2 Market size and forecast, by Type

- 5.2.4.2.3 Market size and forecast, by Application

- 5.2.4.3 Mexico

- 5.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 5.2.4.3.2 Market size and forecast, by Type

- 5.2.4.3.3 Market size and forecast, by Application

- 5.2.4.1 United States

- 5.3 South America

- 5.3.1 Key trends and opportunities

- 5.3.2 Market size and forecast, by Type

- 5.3.3 Market size and forecast, by Application

- 5.3.4 Market size and forecast, by country

- 5.3.4.1 Brazil

- 5.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 5.3.4.1.2 Market size and forecast, by Type

- 5.3.4.1.3 Market size and forecast, by Application

- 5.3.4.2 Argentina

- 5.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 5.3.4.2.2 Market size and forecast, by Type

- 5.3.4.2.3 Market size and forecast, by Application

- 5.3.4.3 Chile

- 5.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.4.3.2 Market size and forecast, by Type

- 5.3.4.3.3 Market size and forecast, by Application

- 5.3.4.4 Rest of South America

- 5.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 5.3.4.4.2 Market size and forecast, by Type

- 5.3.4.4.3 Market size and forecast, by Application

- 5.3.4.1 Brazil

- 5.4 Europe

- 5.4.1 Key trends and opportunities

- 5.4.2 Market size and forecast, by Type

- 5.4.3 Market size and forecast, by Application

- 5.4.4 Market size and forecast, by country

- 5.4.4.1 Germany

- 5.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 5.4.4.1.2 Market size and forecast, by Type

- 5.4.4.1.3 Market size and forecast, by Application

- 5.4.4.2 France

- 5.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 5.4.4.2.2 Market size and forecast, by Type

- 5.4.4.2.3 Market size and forecast, by Application

- 5.4.4.3 Italy

- 5.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 5.4.4.3.2 Market size and forecast, by Type

- 5.4.4.3.3 Market size and forecast, by Application

- 5.4.4.4 United Kingdom

- 5.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.4.4.2 Market size and forecast, by Type

- 5.4.4.4.3 Market size and forecast, by Application

- 5.4.4.5 Benelux

- 5.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 5.4.4.5.2 Market size and forecast, by Type

- 5.4.4.5.3 Market size and forecast, by Application

- 5.4.4.6 Nordics

- 5.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 5.4.4.6.2 Market size and forecast, by Type

- 5.4.4.6.3 Market size and forecast, by Application

- 5.4.4.7 Rest of Europe

- 5.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 5.4.4.7.2 Market size and forecast, by Type

- 5.4.4.7.3 Market size and forecast, by Application

- 5.4.4.1 Germany

- 5.5 Asia Pacific

- 5.5.1 Key trends and opportunities

- 5.5.2 Market size and forecast, by Type

- 5.5.3 Market size and forecast, by Application

- 5.5.4 Market size and forecast, by country

- 5.5.4.1 China

- 5.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 5.5.4.1.2 Market size and forecast, by Type

- 5.5.4.1.3 Market size and forecast, by Application

- 5.5.4.2 Japan

- 5.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 5.5.4.2.2 Market size and forecast, by Type

- 5.5.4.2.3 Market size and forecast, by Application

- 5.5.4.3 India

- 5.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 5.5.4.3.2 Market size and forecast, by Type

- 5.5.4.3.3 Market size and forecast, by Application

- 5.5.4.4 South Korea

- 5.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 5.5.4.4.2 Market size and forecast, by Type

- 5.5.4.4.3 Market size and forecast, by Application

- 5.5.4.5 Australia

- 5.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.4.5.2 Market size and forecast, by Type

- 5.5.4.5.3 Market size and forecast, by Application

- 5.5.4.6 Southeast Asia

- 5.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 5.5.4.6.2 Market size and forecast, by Type

- 5.5.4.6.3 Market size and forecast, by Application

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 5.5.4.7.2 Market size and forecast, by Type

- 5.5.4.7.3 Market size and forecast, by Application

- 5.5.4.1 China

- 5.6 MEA

- 5.6.1 Key trends and opportunities

- 5.6.2 Market size and forecast, by Type

- 5.6.3 Market size and forecast, by Application

- 5.6.4 Market size and forecast, by country

- 5.6.4.1 Middle East

- 5.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 5.6.4.1.2 Market size and forecast, by Type

- 5.6.4.1.3 Market size and forecast, by Application

- 5.6.4.2 Africa

- 5.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 5.6.4.2.2 Market size and forecast, by Type

- 5.6.4.2.3 Market size and forecast, by Application

- 5.6.4.1 Middle East

- 6.1 Overview

- 6.2 Key Winning Strategies

- 6.3 Top 10 Players: Product Mapping

- 6.4 Competitive Analysis Dashboard

- 6.5 Market Competition Heatmap

- 6.6 Leading Player Positions, 2022

7: Company Profiles

- 7.1 Abbott (United States)

- 7.1.1 Company Overview

- 7.1.2 Key Executives

- 7.1.3 Company snapshot

- 7.1.4 Active Business Divisions

- 7.1.5 Product portfolio

- 7.1.6 Business performance

- 7.1.7 Major Strategic Initiatives and Developments

- 7.2 AstraZeneca (United Kingdom)

- 7.2.1 Company Overview

- 7.2.2 Key Executives

- 7.2.3 Company snapshot

- 7.2.4 Active Business Divisions

- 7.2.5 Product portfolio

- 7.2.6 Business performance

- 7.2.7 Major Strategic Initiatives and Developments

- 7.3 Bayer AG (Germany)

- 7.3.1 Company Overview

- 7.3.2 Key Executives

- 7.3.3 Company snapshot

- 7.3.4 Active Business Divisions

- 7.3.5 Product portfolio

- 7.3.6 Business performance

- 7.3.7 Major Strategic Initiatives and Developments

- 7.4 Boehringer Ingelheim International GmbH(Germany)

- 7.4.1 Company Overview

- 7.4.2 Key Executives

- 7.4.3 Company snapshot

- 7.4.4 Active Business Divisions

- 7.4.5 Product portfolio

- 7.4.6 Business performance

- 7.4.7 Major Strategic Initiatives and Developments

- 7.5 Boston Scientific Corporation (United StatesBristolMyers Squibb Company (United States)

- 7.5.1 Company Overview

- 7.5.2 Key Executives

- 7.5.3 Company snapshot

- 7.5.4 Active Business Divisions

- 7.5.5 Product portfolio

- 7.5.6 Business performance

- 7.5.7 Major Strategic Initiatives and Developments

- 7.6 Cook (United Kingdom)

- 7.6.1 Company Overview

- 7.6.2 Key Executives

- 7.6.3 Company snapshot

- 7.6.4 Active Business Divisions

- 7.6.5 Product portfolio

- 7.6.6 Business performance

- 7.6.7 Major Strategic Initiatives and Developments

- 7.7 Edwards Lifesciences Corporation (United States)

- 7.7.1 Company Overview

- 7.7.2 Key Executives

- 7.7.3 Company snapshot

- 7.7.4 Active Business Divisions

- 7.7.5 Product portfolio

- 7.7.6 Business performance

- 7.7.7 Major Strategic Initiatives and Developments

- 7.8 H. Lundbeck A/S (United States)

- 7.8.1 Company Overview

- 7.8.2 Key Executives

- 7.8.3 Company snapshot

- 7.8.4 Active Business Divisions

- 7.8.5 Product portfolio

- 7.8.6 Business performance

- 7.8.7 Major Strategic Initiatives and Developments

- 7.9 Johnson & Johnson Private Limited (United India)

- 7.9.1 Company Overview

- 7.9.2 Key Executives

- 7.9.3 Company snapshot

- 7.9.4 Active Business Divisions

- 7.9.5 Product portfolio

- 7.9.6 Business performance

- 7.9.7 Major Strategic Initiatives and Developments

- 7.10 Merck KGaA (Germany)

- 7.10.1 Company Overview

- 7.10.2 Key Executives

- 7.10.3 Company snapshot

- 7.10.4 Active Business Divisions

- 7.10.5 Product portfolio

- 7.10.6 Business performance

- 7.10.7 Major Strategic Initiatives and Developments

- 7.11 Novartis AG (Switzerland)

- 7.11.1 Company Overview

- 7.11.2 Key Executives

- 7.11.3 Company snapshot

- 7.11.4 Active Business Divisions

- 7.11.5 Product portfolio

- 7.11.6 Business performance

- 7.11.7 Major Strategic Initiatives and Developments

- 7.12 Oxurion NV (Belgium)

- 7.12.1 Company Overview

- 7.12.2 Key Executives

- 7.12.3 Company snapshot

- 7.12.4 Active Business Divisions

- 7.12.5 Product portfolio

- 7.12.6 Business performance

- 7.12.7 Major Strategic Initiatives and Developments

- 7.13 Taxus Cardium Pharmaceuticals Group (CRXM)(United States)

- 7.13.1 Company Overview

- 7.13.2 Key Executives

- 7.13.3 Company snapshot

- 7.13.4 Active Business Divisions

- 7.13.5 Product portfolio

- 7.13.6 Business performance

- 7.13.7 Major Strategic Initiatives and Developments

- 7.14 Vernalis (R&D) Limited (United Kingdom)

- 7.14.1 Company Overview

- 7.14.2 Key Executives

- 7.14.3 Company snapshot

- 7.14.4 Active Business Divisions

- 7.14.5 Product portfolio

- 7.14.6 Business performance

- 7.14.7 Major Strategic Initiatives and Developments

- 7.15 Others

- 7.15.1 Company Overview

- 7.15.2 Key Executives

- 7.15.3 Company snapshot

- 7.15.4 Active Business Divisions

- 7.15.5 Product portfolio

- 7.15.6 Business performance

- 7.15.7 Major Strategic Initiatives and Developments

8: Analyst Perspective and Conclusion

- 8.1 Concluding Recommendations and Analysis

- 8.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the estimated market size of Brain Ischemia in 2030?

+

-

Which type of Brain Ischemia is widely popular?

+

-

What is the growth rate of Brain Ischemia Market?

+

-

What are the latest trends influencing the Brain Ischemia Market?

+

-

Who are the key players in the Brain Ischemia Market?

+

-

How is the Brain Ischemia } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Brain Ischemia Market Study?

+

-

What geographic breakdown is available in North America Brain Ischemia Market Study?

+

-

Which region holds the second position by market share in the Brain Ischemia market?

+

-

How are the key players in the Brain Ischemia market targeting growth in the future?

+

-

,

The market for brain ischaemia is greatly impacted by a number of important drivers that drive its growth and development. First, the rising incidence of cerebrovascular diseases, including stroke and transient ischaemic attacks (TIAs), is a key driver. As these conditions become increasingly prevalent as a result of lifestyle, diet, and physical inactivity, demand for effective diagnostic and therapeutic strategies for brain ischaemia increases proportionally. This increasing pool of patients requires sophisticated medical treatments both for acute conditions and long-term care.

, Secondly, an ageing global population is an equally important factor. Older adults have a higher tendency to contract cerebrovascular disease, hence a major target audience for the brain ischaemia market. With this is added growing awareness about brain ischaemia's risk factors of hypertension, diabetes, hyperlipidaemia, and smoking. Growing public health efforts and educational campaigns are causing earlier diagnosis and active management of such risk factors, further propelling the demand for associated healthcare products and services.