North America Blood Bags Market - Industry Dynamics, Market Size, And Opportunity Forecast To 2030

Report ID: MS-905 | Healthcare and Pharma | Last updated: May, 2025 | Formats*:

Blood bags are sterile, medical-quality bags used for the collection, storage, processing, and transfusion of human blood and its components. Generally made of biocompatible PVC (polyvinyl chloride) or other modern polymers, the bags provide the stability and viability of the blood products by protecting them from contamination and providing ideal storage conditions. They come in a range of configurations, such as one bag for the collection of whole blood and multi-bag systems (double, triple, or quadruple) for blood separation into its components, such as red blood cells, plasma, and platelets, maximising their application and shelf life.

The market of blood bags includes the production and distribution of these critical medical devices to blood banks, hospitals, and healthcare facilities across the globe. Growth in the market is fuelled by an ongoing demand for blood transfusions as a result of surgeries, trauma, chronic illnesses, and other medical conditions necessitating blood component therapy.

Blood Bags Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

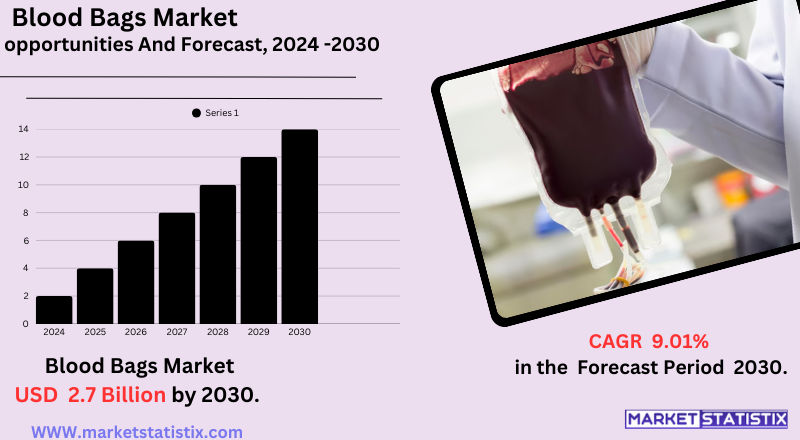

| Growth Rate | CAGR of 9.01% |

| Forecast Value (2030) | USD 2.7 Billion |

| By Product Type | Single Collection, Double Collection, Triple Collection, Quadruple Collection, Others |

| Key Market Players |

|

| By Region |

|

Blood Bags Market Trends

One of the important trends is moving towards technology-enabled blood bags with features such as built-in filters for leukocyte reduction, enhanced sealing technology, and ergonomic handling that makes them simpler to use. There's also increased implementation of intelligent technologies like RFID-based traceability and barcode scanning software that enable end-to-end tracking of blood units from donor to patient, reducing errors and improving inventory control in blood banks and hospitals.

Another trend of note is growing demands for multi-bag systems (triple and quadruple bags) that enable whole blood separation into its multiple components (red blood cells, plasma, and platelets). This enables efficient use of a single donation and provides component therapy, which is increasingly popular in contemporary clinical practices. In addition, advances in blood preservative solutions and cryopreservation methods are increasing the shelf life of blood products, particularly for rare-type blood and specialised products.

Blood Bags Market Leading Players

The key players profiled in the report are AdvacarePharma (United States), Fresenius Kabi (Germany)HLL Lifecare Limited (India), TERUMO (Japan), Span Healthcare Private Limited (India), INNVOL Medical India Limited (India), Poly Medicure Limited (India), Velico Medical, Inc. (United States)Growth Accelerators

The market for blood bags is most influenced by the surging demand for blood and blood components across the world that is triggered by an escalating number of surgeries and a growing prevalence of chronic diseases that require blood transfusions. Regular blood product therapy often becomes mandatory for disorders such as cancer, anaemia, and haemophilia, thereby leading straight to an enhanced demand for blood bags in clinics and hospitals. Also, the rising incidence of trauma cases and road traffic accidents worldwide further adds to the ongoing need for blood transfusions, thus supporting the market for blood bags.

Technological advancements like multi-chamber bags that facilitate effective separation of blood components (red cells, plasma, platelets) for specific therapies and the production of safer materials such as DEHP-free and PVC-free bags improve product safety and shelf life. In addition, advances in the sterilisation process, incorporation of smart technologies such as RFID tracking to improve traceability, and automated blood processing systems are propelling the use of advanced blood bags to safer and more efficient blood management practices globally.

Blood Bags Market Segmentation analysis

The North America Blood Bags is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Single Collection, Double Collection, Triple Collection, Quadruple Collection, Others . The Application segment categorizes the market based on its usage such as Hospitals and Clinics, Blood Banks, Other. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

Recent acquisitions and mergers in the blood bags industry demonstrate a trend towards global expansion and innovation. Maco Pharma signed a partnership deal with China's Tianhe Pharmaceutical in December 2022 for co-manufacturing blood bags with the aim of enhancing its presence in the Asian market. Likewise, Terumo Blood and Cell Technologies acquired a $10.6 million contract in April 2022 from the U.S. Medical Technology Enterprise Consortium (MTEC) to develop freeze-dried plasma technologies, marking the transition to next-generation blood storage products.

Large industry players such as Grifols and Haemonetics have also been involved in acquisitions to strengthen their hand. Grifols has also strengthened its international presence through plasma collection network acquisitions and strategic partnerships within geographies such as Egypt and China. Haemonetics acquired Attune Medical for $160 million in April 2024, which adds temperature control technologies that are essential for the management of blood to its portfolio. These initiatives reflect a larger industry movement of using mergers and acquisitions to stimulate innovation, broaden market access, and address changing healthcare needs.

Challenges In Blood Bags Market

The market for blood bags has serious challenges, the majority of which are rooted in tight regulatory conditions and the necessity for strict quality control. Companies have to meet intricate and dynamic criteria outlined by regulators like the FDA and the EMA, requiring extensive validation, testing, and following Good Manufacturing Practices (GMP). The regulatory pressures raise the costs of production, extend the time taken to develop products, and can serve as entry barriers to the market for new entrants.

A further significant challenge is the persistent risk of contamination and disease transmission through blood collection, storage, and transfusion, necessitating ongoing investment in sophisticated safety measures and sterilising technologies. The expense of installing automated and technologically sophisticated blood collection systems can be very high, particularly for healthcare centers in low- and middle-income countries. All these challenges cumulatively necessitate strategic investments in research, compliance, and innovation to provide both patient protection and market competitiveness.

Risks & Prospects in Blood Bags Market

The use of biodegradable plastics and technologies in blood storage, including polymer-based bags that increase blood shelf life, are also creating new opportunities for market growth. Also contributing is increasing awareness and voluntary participation in blood donation drives, which are enhancing collected blood availability, prompting investments in quality and high-tech blood storage products.

Region-wise, the market is led by North America based on its established health infrastructure, regulatory environment, and high demand for blood products in specialised medical treatment. Europe comes next with a rising population base and increasing medical procedures, especially in countries such as Germany. The Asia Pacific market is likely to witness the highest growth, with a CAGR of more than 8% between 2025 and 2030, driven by extensive public health programmes, growing healthcare infrastructure, and government-supported reforms in nations like India, China, and the Philippines. These markets are increasingly boosting purchasing of advanced and cost-effective blood bag systems to address increasing urban and rural health demands.

Key Target Audience

,Furthermore, the market is regulated by government health ministries, non-government organizations (NGOs), and global health organizations that aid blood donation activities and blood bank infrastructure development, especially in the developing world. They have a key role to play in increasing access to blood transfusion services and improving the efficiency and safety of blood collection and storage. The increasing consciousness and voluntary blood donation campaigns, coupled with the rising incidence of blood disorders and the growing rate of road accidents, are further driving the growth of the market.

,The primary market for blood bags consists of hospitals, clinics, and blood banks, the largest consumers because of their key roles in storing, collecting, and transfusing blood. The market share of the hospital and clinic is a major proportion, fuelled by the growing number of surgical operations, trauma cases, and treatments of chronic diseases that involve blood transfusion. Blood banks also contribute a significant share of the market since they are at the core of blood donation collection and processing. The demand for these end-users is additionally boosted by requiring secure and effective blood storage systems, compliance with very stringent regulatory requirements, and the incorporation of sophisticated technologies to enable traceability of blood and inventory management.

,, ,,

Merger and acquisition

Recent acquisitions and mergers in the blood bags industry demonstrate a trend towards global expansion and innovation. Maco Pharma signed a partnership deal with China's Tianhe Pharmaceutical in December 2022 for co-manufacturing blood bags with the aim of enhancing its presence in the Asian market. Likewise, Terumo Blood and Cell Technologies acquired a $10.6 million contract in April 2022 from the U.S. Medical Technology Enterprise Consortium (MTEC) to develop freeze-dried plasma technologies, marking the transition to next-generation blood storage products.

Large industry players such as Grifols and Haemonetics have also been involved in acquisitions to strengthen their hand. Grifols has also strengthened its international presence through plasma collection network acquisitions and strategic partnerships within geographies such as Egypt and China. Haemonetics acquired Attune Medical for $160 million in April 2024, which adds temperature control technologies that are essential for the management of blood to its portfolio. These initiatives reflect a larger industry movement of using mergers and acquisitions to stimulate innovation, broaden market access, and address changing healthcare needs.

Analyst Comment

The blood bags market is growing steadily, with an estimated market size in 2025 being around USD 367 million to USD 489 million, and projections seeing the market reaching USD 527 million to USD 637 million by the years 2030-2033. The growth is fuelled by the increasing demand for blood transfusions, which is boosted by the growing number of surgeries, trauma injuries, chronic illnesses, and an ageing global population. Hospitals and clinics are still the biggest consumers, capturing almost half of the market share, as they use blood bags in life-saving procedures like chemotherapy, organ transplants, and emergency treatment.

- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Blood Bags- Snapshot

- 2.2 Blood Bags- Segment Snapshot

- 2.3 Blood Bags- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Blood Bags Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Single Collection

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Double Collection

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Triple Collection

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Quadruple Collection

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

- 4.6 Others

- 4.6.1 Key market trends, factors driving growth, and opportunities

- 4.6.2 Market size and forecast, by region

- 4.6.3 Market share analysis by country

5: Blood Bags Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Hospitals and Clinics

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Blood Banks

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Other

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Blood Bags Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 AdvacarePharma (United States)

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Fresenius Kabi (Germany)HLL Lifecare Limited (India)

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 INNVOL Medical India Limited (India)

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Poly Medicure Limited (India)

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Span Healthcare Private Limited (India)

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 TERUMO (Japan)

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Velico Medical

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Inc. (United States)

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Blood Bags in 2030?

+

-

Which application type is expected to remain the largest segment in the North America Blood Bags market?

+

-

How big is the North America Blood Bags market?

+

-

How do regulatory policies impact the Blood Bags Market?

+

-

What major players in Blood Bags Market?

+

-

What applications are categorized in the Blood Bags market study?

+

-

Which product types are examined in the Blood Bags Market Study?

+

-

Which regions are expected to show the fastest growth in the Blood Bags market?

+

-

Which application holds the second-highest market share in the Blood Bags market?

+

-

What are the major growth drivers in the Blood Bags market?

+

-

The market for blood bags is most influenced by the surging demand for blood and blood components across the world that is triggered by an escalating number of surgeries and a growing prevalence of chronic diseases that require blood transfusions. Regular blood product therapy often becomes mandatory for disorders such as cancer, anaemia, and haemophilia, thereby leading straight to an enhanced demand for blood bags in clinics and hospitals. Also, the rising incidence of trauma cases and road traffic accidents worldwide further adds to the ongoing need for blood transfusions, thus supporting the market for blood bags.

Technological advancements like multi-chamber bags that facilitate effective separation of blood components (red cells, plasma, platelets) for specific therapies and the production of safer materials such as DEHP-free and PVC-free bags improve product safety and shelf life. In addition, advances in the sterilisation process, incorporation of smart technologies such as RFID tracking to improve traceability, and automated blood processing systems are propelling the use of advanced blood bags to safer and more efficient blood management practices globally.