Global Standardized Cork Packaging Market – Industry Trends and Forecast to 2030

Report ID: MS-2127 | Food and Beverages | Last updated: Dec, 2024 | Formats*:

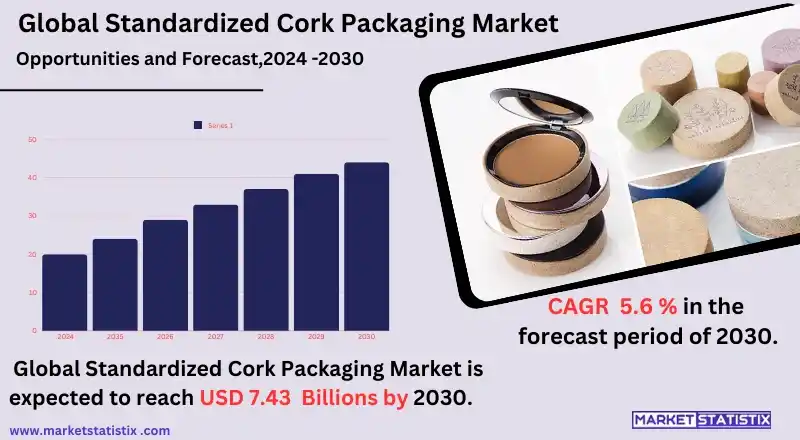

Standardized cork packaging Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 5.6% |

| Forecast Value (2030) | USD 7.43 Billion |

| By Product Type | Natural Cork, Polymerized Cork, Composite Cork |

| Key Market Players |

|

| By Region |

|

Standardized cork packaging Market Trends

The standardized cork packaging market is currently undergoing a transformation as the focus has shifted towards the application of green and sustainable alternatives owing to the increasing consumer crowd for environmentally friendly products. Cork, being a renewable, biodegradable, and recyclable material, is increasingly being embraced as a better packaging option in the food and beverage, cosmetics, and wine sectors. More and more brands are opting to use cork packaging in order to meet their sustainability targets, cut their greenhouse gas emissions, and target consumers who want to replace plastics and synthetics with natural, recyclable materials. Moreover, the market is also expanding in the form of decorative designs of cork-based packaging, as the manufacturers are emphasizing the functional and artistic aspects of cork-based products as well. Due to this increasing competition, more and more companies are opting for customized cork packing solutions to stand out in the market. The trend of using cork for packaging also extends to the use of luxury packaging, where it is used in the packaging of high-end wines and aged spirits designed to offer a more genuine feel to the customers.Standardized cork packaging Market Leading Players

The key players profiled in the report are GAP Packaging, Jelinek Cork Group, Pace Products LLC, Teals Prairie and Co., Amorim Cork America, Sugherificio Martinese & Figli Srl, Bangor Cork, Fudy Solutions Inc, PORTOCORK AMERICA, HZ cork, Korkindustrie GmbH & Co. KG, HELIX, Advance Cork International, J. C. RIBEIRO, Cutting Edge Converted Products, Diam Bouchage SAS, WidgetCo, Berlin Packaging, M. A. Silva, Lafitte Cork GroupGrowth Accelerators

The need for cork packaging solutions in the market at present is because of the growing preference for sustainable, user-friendly, and cost-effective packaging solutions in almost every sector. With a growing number of individuals and companies becoming eco-friendly, cork, which is a natural, plant-based material that is renewable and decomposable, has found its way into packaging, especially in wine, cosmetics, and food. Primarily, cork has gained notoriety in the advancement of sustainable packaging due to its desirable characteristics like aesthetic value, light weight, and durability, despite the fact that it can be recycled, making it more preferred than plastic and other harmful packaging materials. Another key driver is the growing trend of premium and luxury packaging. Cork packing is closely associated with expensive items, as this substance has distinct and beautiful fabrics that add value to the products and improve customer satisfaction. Cork sheath packaging is now increasingly adopted in the food and spirit segment, beauty products such as packaging and capping services, and more for the structure of the designs as well as meeting the customers’ needs for luxurious, uniquely textured packages. We expect this new development in packaging concepts to sustain the growth of the target market.Standardized cork packaging Market Segmentation analysis

The Global Standardized cork packaging is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Natural Cork, Polymerized Cork, Composite Cork . The Application segment categorizes the market based on its usage such as Food and Beverages, Cosmetics and Personal care, Others. Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The standardized cork packaging market has a fair share of both global and regional players, and companies have managed to sustain a competitive advantage through innovation and sustainability. The key players in those markets are more frequently adopting green practices and promoting the packaging solutions based on green renewable cork material. While companies Amorim Cork Composites and Cork Supply are the main companies in charge of cork-based packaging products, they owe this to their long history in cork acquisition, treatment, and designing. Environmental considerations such as biodegradability and low carbon emissions are given special consideration since most of the industries and consumers are in search of more sustainable options than plastic and other traditional packaging materials. More than just the big players, there is also an increasing presence of small and medium enterprises (SMEs) that are coming up with the targeted designs of cork packaging systems for selected sectors like the luxury product markets, such as wines, spirits, and cosmetics. These companies are differentiating themselves by providing different designs and high levels of served customer customization, as there is high demand for environmentally friendly and beautifully packaged products.Challenges In Standardized cork packaging Market

The standardized cork packaging market is encountering various obstacles regarding the availability and cost of the raw materials. This is partly because cork is a natural product, and its manufacturing is dependent on certain climatic conditions and harvesting techniques, which may cause disruptions in the supply chain and cause fluctuations in prices. Another challenge is that hassle-free and cheap alternatives such as plastics, glass, and cardboard pose a competition to cork packaging. However, in some low-cost markets, the higher price of sustainable cork-based packaging, as opposed to synthetic packaging materials, may restrict the use of organic requirements.Risks & Prospects in Standardized cork packaging Market

The market for tailored cork packaging has enormous potential owing to the increase in demand for new-age green packaging materials. Everyone from end-users to companies is becoming obsessed with the environmental crisis, thus providing a perfect option for cork, as it is a natural material that is renewable and biodegradable, unlike all the other toxic materials such as plastics and other non-biodegradable products. Be it food and beverage industries, cosmetics, or wine packaging, every other industry has started embracing standardized cork packaging in order to respond to the request for environmentally friendly products from consumers as well as the initiatives aimed at minimizing the use of polythene bags. In addition, the increased concern for package aesthetics, especially for product categories such as wines, premium products, and organic beauty products, represents a vital opportunity for the growth of the standardized cork packaging. The texture and appearance of cork enhance the look of the product, so it is fit for use in high-end packages. Whereas many brands have adopted sustainability as the concept to take up in the cutthroat markets that they operate in, bespoke cork packaging systems have an aesthetic touch, but they can also offer functional roles such as a moisture barrier and protection of packed items. Such excitement can lead to more resource engagement and growth in the cork-based packing market.Key Target Audience

The main organizations targeted for the market of standardized cork packaging are those engaged in the manufacture and supply of wines and spirits, food, and cosmetics, respectively. Cork is a green and high-end packaging material usually associated with wine bottles as it replaces synthetic closures while maintaining product quality. Therefore, winemakers and vodka producers embrace corking, as its elements help seal the contained product naturally and, at the same time, are attractive to the consumers. In addition, food and cosmetic industries also use cork in the packing of high-end goods, where eco-friendly and visually appealing packaging assists in building brand equity and targeting the green segment of the market.,, The other significant segment comprises end users and retailers who are ecologically oriented and seek green packaging. Owing to the increasing awareness among people about the environment, a number of brands have incorporated cork packaging into their products to show their stand on plastic waste and carbon emissions. In addition, retailers, especially in the premium and luxury markets, also advocate for cork packaging to suit the market of non-plastic renewable materials.Merger and acquisition

The cork packaging market in its standardized form has recently experienced an upsurge in the movement concerning mergers and acquisitions, which is indicative of the growth of the sector and the rising need for environmentally friendly packaging. Early in the year 2024, in raised capital transactions, take, for instance, the acquisition of AmeriPac by Veritiv, aimed at broadening its portfolio of services in contract packaging, which is in line with the growing need for green packing methods. The active tsunami of mergers and purchases within the industry is being experienced by companies like Jelinek Cork Group and Amorim Cork America, who are on the inside, ready to form new alliances and buy out for an extension of their market share. Furthermore, there is a great emphasis from the market players on innovations and the sustainability of cork in developing the packaging solutions, which also affects the combination of competitors. Part of the motivation behind acquisition policies is to increase the production capacity and level of vertical integration of product offerings in response to changing consumer preferences. For example, as brands built to last focus on sustainability more than ever before, cork's natural properties make it a viable option for packaging materials for a range of luxury goods, particularly in the barrel sector of the wine market.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Standardized cork packaging- Snapshot

- 2.2 Standardized cork packaging- Segment Snapshot

- 2.3 Standardized cork packaging- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Standardized cork packaging Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Natural Cork

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Polymerized Cork

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Composite Cork

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

5: Standardized cork packaging Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Food and Beverages

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Cosmetics and Personal care

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Others

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Standardized cork packaging Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 GAP Packaging

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Jelinek Cork Group

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Pace Products LLC

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Teals Prairie and Co.

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Amorim Cork America

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Sugherificio Martinese & Figli Srl

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Bangor Cork

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Fudy Solutions Inc

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 PORTOCORK AMERICA

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 HZ cork

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Korkindustrie GmbH & Co. KG

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 HELIX

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Advance Cork International

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 J. C. RIBEIRO

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

- 8.15 Cutting Edge Converted Products

- 8.15.1 Company Overview

- 8.15.2 Key Executives

- 8.15.3 Company snapshot

- 8.15.4 Active Business Divisions

- 8.15.5 Product portfolio

- 8.15.6 Business performance

- 8.15.7 Major Strategic Initiatives and Developments

- 8.16 Diam Bouchage SAS

- 8.16.1 Company Overview

- 8.16.2 Key Executives

- 8.16.3 Company snapshot

- 8.16.4 Active Business Divisions

- 8.16.5 Product portfolio

- 8.16.6 Business performance

- 8.16.7 Major Strategic Initiatives and Developments

- 8.17 WidgetCo

- 8.17.1 Company Overview

- 8.17.2 Key Executives

- 8.17.3 Company snapshot

- 8.17.4 Active Business Divisions

- 8.17.5 Product portfolio

- 8.17.6 Business performance

- 8.17.7 Major Strategic Initiatives and Developments

- 8.18 Berlin Packaging

- 8.18.1 Company Overview

- 8.18.2 Key Executives

- 8.18.3 Company snapshot

- 8.18.4 Active Business Divisions

- 8.18.5 Product portfolio

- 8.18.6 Business performance

- 8.18.7 Major Strategic Initiatives and Developments

- 8.19 M. A. Silva

- 8.19.1 Company Overview

- 8.19.2 Key Executives

- 8.19.3 Company snapshot

- 8.19.4 Active Business Divisions

- 8.19.5 Product portfolio

- 8.19.6 Business performance

- 8.19.7 Major Strategic Initiatives and Developments

- 8.20 Lafitte Cork Group

- 8.20.1 Company Overview

- 8.20.2 Key Executives

- 8.20.3 Company snapshot

- 8.20.4 Active Business Divisions

- 8.20.5 Product portfolio

- 8.20.6 Business performance

- 8.20.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Standardized cork packaging in 2030?

+

-

How big is the Global Standardized cork packaging market?

+

-

How do regulatory policies impact the Standardized cork packaging Market?

+

-

What major players in Standardized cork packaging Market?

+

-

What applications are categorized in the Standardized cork packaging market study?

+

-

Which product types are examined in the Standardized cork packaging Market Study?

+

-

Which regions are expected to show the fastest growth in the Standardized cork packaging market?

+

-

What are the major growth drivers in the Standardized cork packaging market?

+

-

Is the study period of the Standardized cork packaging flexible or fixed?

+

-

How do economic factors influence the Standardized cork packaging market?

+

-