Global Proteomics Market - Industry Dynamics, Market Size, And Opportunity Forecast To 2030

Report ID: MS-2581 | Chemicals And Materials | Last updated: May, 2025 | Formats*:

The proteomics industry involves the research, production, and distribution of equipment and technology employed to examine the structure, function, and interactions of proteins in biological systems. Proteins are cellular workhorses involved in virtually every biological process. Proteomics is focused on gaining insight into the complete set of proteins produced by an organism, tissue, or cell at any given moment and their modifications, interactions, and abundance. This discipline employs a variety of advanced methods like mass spectrometry, protein microarrays, electrophoresis, chromatography, and bioinformatics tools for protein identification, quantitation, and characterisation.

The proteomics industry is fuelled by the growing demand to comprehend the molecular basis of diseases, identify novel drug targets, and create personalised medicine strategies. It is crucial in numerous applications, such as biomarker discovery for the detection of diseases at an early stage, drug discovery and toxicology research, agricultural biotechnology for crop enhancement, and basic biological research to understand basic cellular processes.

Proteomics Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

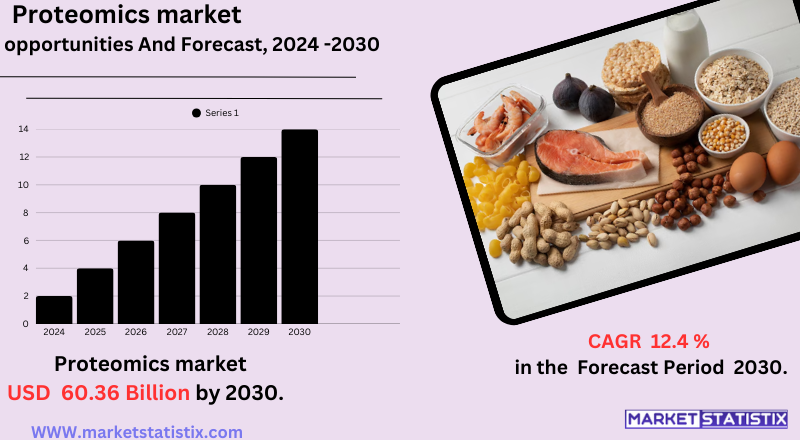

| Growth Rate | CAGR of 12.4% |

| Forecast Value (2030) | USD 60.36 Billion |

| By Product Type | Instruments, Reagents & Consumables, Services |

| Key Market Players |

|

| By Region |

|

Proteomics Market Trends

The proteomics market is going through strong growth and is dominated by a number of key trends. One of the biggest drivers is the need for personalised medicine, where proteomics is critical in the identification of biomarkers, drug targets, and treatment response monitoring at the molecular level, resulting in customized therapies. The market is also driven by the increasing uses of proteomics in drug discovery and development, facilitating target identification, drug mechanism understanding, and drug safety assessment.

Technological innovations are at the core of these trends. Advances in mass spectrometry, especially high-resolution and high-throughput instruments, are improving the accuracy and speed of protein analysis. The convergence of bioinformatics and artificial intelligence (AI) is increasingly crucial for handling and understanding the extensive and complex datasets produced in proteomics research. Additionally, the emergence of multi-omics approaches, integrating proteomics with genomics, transcriptomics, and metabolomics, offers a holistic knowledge of biological systems, spurring advances in both research and clinical diagnostics, such as early disease detection and diagnostics.

Proteomics Market Leading Players

The key players profiled in the report are Waters Corporation, Danaher, Bruker Corporation, Thermo Fisher Scientific, Inc., Merck KGaA, Agilent Technologies, Inc., Illumina, Inc., Bio-Rad Laboratories, Inc., F. Hoffmann-La Roche Ltd., Standard BioTools Inc.Growth Accelerators

The proteomics market is largely driven by the growing demand for personalised medicine. Proteomics offers vital molecular-level insights that make it possible to identify specific biomarkers, drug targets, and therapeutic responses, allowing for personalised treatments against diseases such as cancer and neurological disorders. The growing incidence of chronic diseases worldwide also accelerates this demand, as proteomics helps one understand the mechanisms behind the diseases and create more efficient diagnostic and therapeutic approaches.

Another major push factor is the ongoing improvement in proteomics technologies, especially mass spectrometry and bioinformatics. Developments to increase sensitivity, precision, and capacity in protein examination are empowering scientists to better explore intricate biological systems. The use of artificial intelligence and machine learning tools to interpret data is also transforming biomarker discovery and drug development workflows.

Proteomics Market Segmentation analysis

The Global Proteomics is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Instruments, Reagents & Consumables, Services . The Application segment categorizes the market based on its usage such as Drug Discovery, Clinical Diagnostics, Others. Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The competitive market structure of the proteomics industry is dominated by large incumbent players and an increasing number of specialised and innovative firms. The major world leaders are Thermo Fisher Scientific, Agilent Technologies, Danaher Corporation (SCIEX), Merck KGaA, and Bio-Rad Laboratories. These players provide a complete line of instruments (e.g., mass spectrometers and chromatography systems), reagents, software, and services that span the complete proteomics workflow. Their large product ranges, good R&D strengths, and extensive geographical presence give them a strong competitive edge.

But the market also includes growing competition from niche firms and startups operating in niche technologies or applications. Firms like Bruker Corporation, Illumina (combining genomics and proteomics), and new entrants like Pixelgen Technologies (spatial proteomics) and Alamar Biosciences (precision proteomics) are presenting novel solutions. Competition is building up through technical innovations, like increased-sensitivity mass spectrometry, sophisticated bioinformatics tools, and the design of integrated multi-omics platforms.

Challenges In Proteomics Market

The proteomics industry is challenged mainly by the prohibitive expense of high-end equipment and technology, including mass spectrometers and chromatographic instrumentation. The advanced equipment demands huge initial capital expenditure and is not readily affordable by small and medium-sized companies and research institutions. Subsequent expenses on reagents, upkeep, and specialised personnel also contribute to added expenses, delimiting wider application and hindering market development, particularly in developing markets.

A significant challenge is the data management and analysis complexity. Proteomics research yields high volumes of data that are highly specialised in terms of requiring sophisticated expertise and bioinformatics software to process and interpret. A lack of uniform data formats, data platform interoperability, and streamlined data management systems frequently contributes to research delays, impedes biomarker identification, and complicates regulatory submissions. These challenges are complicated by variability in sample preparation, restricted reproducibility across laboratories, and changing regulatory needs, all of which can hinder the translation of proteomics discoveries into clinics and commerce.

Risks & Prospects in Proteomics Market

Major market opportunities are the growing incidence of infectious and chronic diseases, advances in protein analysis technology, and the growing uses of proteomics in medicine and agriculture. Advances like mass spectrometry and top-down proteomics are facilitating high-throughput analysis, closing the gap between phenotypes and genotypes, and aiding the creation of targeted therapies for diseases such as cancer and diabetes.

Regionally, North America dominates the market on account of robust research funding, a strong pharmaceutical and biotech sector, and early embrace of advanced technologies, with the U.S. generating more than 40% of worldwide revenue. Europe comes next, driven by government-supported scholarly initiatives and a large healthcare industry. The Asia-Pacific region, led by China and India, will see the most rapid expansion, driven by its fast industrialisation, expansion of healthcare expenditure, and substantial government and private investments in research and development. China leads particularly strongly with its vigorous investment in biotechnology and precision medicine as a regional leader.

Key Target Audience

The market for proteomics targets mainly pharmaceutical and biotech firms, academic and research institutes, and healthcare providers. Biotech and pharmaceutical companies apply proteomics to drug discovery and targeted medicine uses, using protein analysis to discover new drug targets and create customized treatments. Academic and research organizations pursue the development of proteomic technology and methods to better understand protein function and interaction. Healthcare professionals embrace proteomic technologies for patient care and clinical diagnostics with an objective to improve disease diagnosis and treatment approaches. Also, contract research organizations (CROs) and diagnostic labs are notable segments of the proteomics market.

,

, CROs provide focused proteomic services to aid pharmaceutical and biotechnology firms in their research and development process so as to make the studies efficient and economical. Diagnostic laboratories utilise proteomic analyses to create and apply sophisticated diagnostic tests, enhancing the speed and accuracy of disease diagnosis. The application of proteomics in these industries highlights its growing significance in contemporary biomedical research and clinical practice.

Merger and acquisition

The proteomics industry has seen high levels of merger and acquisition activity over the past few years, with a trend toward consolidation and the expansion of technology capabilities. Thermo Fisher Scientific acquired Olink Holding AB for $3.1 billion in 2024, strengthening its leadership in high-throughput proteomics solutions. Olink's advanced proteomics discovery expertise benefits both academic institutions and biopharma organizations. In 2023, Danaher Corporation bought Abcam for around $5.7 billion, bolstering its proteomics tools and reagents portfolio. Moreover, SomaLogic merged with Standard BioTools in an all-stock transaction, forming a diversified life sciences tools leader.

Strategic partnerships have also been important in the development of proteomics technologies. Bruker Corporation and Biognosys AG entered into collaboration in 4D proteomics technology with a view to propelling high-precision proteomics research. In addition, Alamar Biosciences introduced the NULISAseq CNS Disease Panel 120 in 2024 for neurological disorders and collaborated with Biognosys to provide these assays. All these developments highlight an active and fast-paced proteomics environment that is propelled by strategic mergers, acquisitions, and collaborations.

Analyst Comment

The proteomics market around the world is growing at a fast pace, with estimates putting it to rise from approximately $44.8 billion in 2025 to $134.8 billion in 2035. This expansion is driven by increased demand for personalised medicine, more investment in drug discovery, and advances in protein analysis technologies, especially mass spectrometry and bioinformatics software. Proteomics is of vital importance in the detection of disease at an early stage, personalised medicines, and the creation of targeted medicines for diseases such as cancer and diabetes and applications in agriculture to improve crops.mics market.

- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Proteomics- Snapshot

- 2.2 Proteomics- Segment Snapshot

- 2.3 Proteomics- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Proteomics Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Instruments

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Reagents & Consumables

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Services

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

5: Proteomics Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Drug Discovery

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Clinical Diagnostics

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Others

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Proteomics Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Illumina

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Inc.

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Agilent Technologies

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Inc.

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Bio-Rad Laboratories

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Inc.

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Thermo Fisher Scientific

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Inc.

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Bruker Corporation

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 F. Hoffmann-La Roche Ltd.

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Waters Corporation

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Merck KGaA

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Danaher

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 Standard BioTools Inc.

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Proteomics in 2030?

+

-

How big is the Global Proteomics market?

+

-

How do regulatory policies impact the Proteomics Market?

+

-

What major players in Proteomics Market?

+

-

What applications are categorized in the Proteomics market study?

+

-

Which product types are examined in the Proteomics Market Study?

+

-

Which regions are expected to show the fastest growth in the Proteomics market?

+

-

Which application holds the second-highest market share in the Proteomics market?

+

-

What are the major growth drivers in the Proteomics market?

+

-

The proteomics market is largely driven by the growing demand for personalised medicine. Proteomics offers vital molecular-level insights that make it possible to identify specific biomarkers, drug targets, and therapeutic responses, allowing for personalised treatments against diseases such as cancer and neurological disorders. The growing incidence of chronic diseases worldwide also accelerates this demand, as proteomics helps one understand the mechanisms behind the diseases and create more efficient diagnostic and therapeutic approaches.

Another major push factor is the ongoing improvement in proteomics technologies, especially mass spectrometry and bioinformatics. Developments to increase sensitivity, precision, and capacity in protein examination are empowering scientists to better explore intricate biological systems. The use of artificial intelligence and machine learning tools to interpret data is also transforming biomarker discovery and drug development workflows.

Is the study period of the Proteomics flexible or fixed?

+

-