Global Peritoneal Dialysis Market – Industry Trends and Forecast to 2030

Report ID: MS-940 | Healthcare and Pharma | Last updated: May, 2025 | Formats*:

The peritoneal dialysis (PD) market includes a global industry dedicated to providing products and services for peritoneal dialysis, a renal replacement therapy that is used for patients with end-phase renal disease (ESRD) or acute renal injury. In PD, the peritoneum, the abdominal lining, acts as a natural filter. A sterile dialysis solution is introduced into the peritoneal cavity through a catheter, where it lasts for a period, absorbing extra fluids from waste products and blood. This solution is then dried and discarded.

The market includes essential components such as peritoneal dialysis solutions (dilsets), peritoneal dialysis cycles (machines for automatic PDs), catheters and transfer sets. The market is mainly inspired by increasing global proliferation of ESRD, often associated with increasing rates of diabetes and high blood pressure. A significant advantage of peritoneal dialysis is its flexibility, as it can often be done by patients at home, offers more freedom and reduces the need for frequent visits to dialysis centers to haemodialysis.

Peritoneal Dialysis Report Highlights

| Report Metrics | Details |

|---|---|

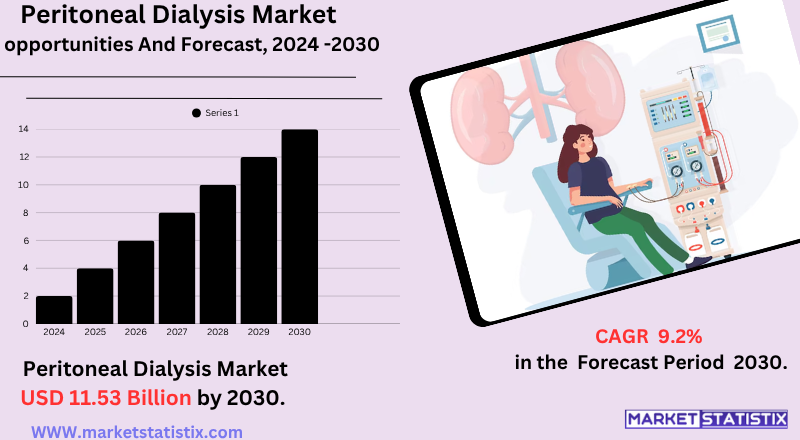

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 9.2% |

| Forecast Value (2030) | USD 11.53 Billion |

| By Product Type | CAPD, APD |

| Key Market Players |

|

| By Region |

|

Peritoneal Dialysis Market Trends

The peritoneal dialysis (PD) market is currently experiencing a strong change towards home-based care, as well as many major trends operated by the growing global burden of chronic kidney disease (CKD) and end-stage renal disease (ESRD). There is a significant increase in the adoption of automatic peritoneal dialysis (APD) systems, which allow patients to do dialysis overnight during sleep, which continuously offers more convenience, flexibility and better quality of life than continuous ambulatory peritoneal dialysis (CAPD). This priority for home-based treatment is supported by government initiatives and reimbursement policies in various countries, aimed at promoting self-care and reducing health care costs associated with in-centre remedies.

Technological progression is also a major trend in which biocompatible dialysis solutions are designed to reduce peritoneal membrane damage with innovations and reduce side effects, which improves long-term patient results. The integration of telemedicine and remote monitoring technologies is revolutionising PD management, allowing healthcare providers to track patient data from far away, provide timely intervention and provide virtual counselling.

Peritoneal Dialysis Market Leading Players

The key players profiled in the report are Medical Components, Inc., Cook Medical Inc., Glomeria Therapeutics, Baxter International Inc., Utah Medical Products, Inc., CardioMed Supplies, Inc., Fresenius Kabi AG, Poly Medicure Ltd., Medtronic, Other playersGrowth Accelerators

The peritoneal dialysis (PD) market is powered by several major factors. A primary driver is the increasing global prevalence of end-stage renal disease (ESRD), which is often the result of the increasing incidence of chronic conditions such as diabetes and high blood pressure. Since the number of patients requiring renal replacement therapy is increasing, the demand for effective dialysis solutions, a viable and often preferred option for many with PDs, is offered. Additionally, the population of growing agers worldwide is an important contributor, as older people are susceptible to kidney-related disorders and can prefer the low-disruptive nature of home-based PDs.

Another important market driver is the increasing preference for home-based dialysis treatment. Peritoneal dialysis provides patients more flexibility, freedom and a better quality of life than in-centre haemodialysis, as it can be done in the comfort of their own homes. This change is further supported by technological progress in PD devices, such as more portable automated peritoneal dialysis (APD) cycles and remote monitoring systems, which increase home remedies and efficiency.

Peritoneal Dialysis Market Segmentation analysis

The Global Peritoneal Dialysis is segmented by Type, Application, and Region. By Type, the market is divided into Distributed CAPD, APD . The Application segment categorizes the market based on its usage such as Home health care, Hospitals and Others. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

Peritoneal dialysis (PD) is dominated by some global players and regional manufacturers in the competitive landscape of the market. Baxter International Inc. and Fresenius Medical Care AG and Company are undisputed leaders who hold important market share. They take advantage of their comprehensive product portfolio, including PD solutions, cyclers for automated peritoneal dialysis (APD), and catheters, as well as their global distribution network and strong R&D abilities. These companies focus on constant innovation, which develops more advanced and user-friendly home-based PD systems to meet the growing preference for self-care and distance monitoring.

Beyond these veterans, among other notable players, B. Braun Melsungen AG, the Dnipro Corporation and Medtronic PLC (with Ligi PD assets) are included. Regional players, especially in the Asia-Pacific region, also contribute to the market, often competing on cost-effect and local solutions. Major competitive strategies revolve around technological progress (e.g., portable cycles, better dialysis solutions, distance patient monitoring), expanding the appearance in emerging markets where ESRD is increasing, and securing favourable reimbursement policies.

Challenges In Peritoneal Dialysis Market

The peritoneal dialysis market faces many frequent challenges that limit its widespread adoption and growth, especially in lower- and medium-orientated countries. Major obstacles include high treatment costs, limited awareness and education due to eggs and trained nephrologists and healthcare staff. In many areas, the cost of peritoneal dialysis – especially for fluids and automated equipment – is prohibitive for both patients and health care systems, often more than the cost of haemodialysis.

Clinical challenges also persist, there are notable risks with peritonalis and mechanical failures associated with peritoneal dialysis that affect the patient's consequences and affect adoption. These complications, coupled with standardized training and limited government reimbursement in some areas, contribute to low global use rates - only 11% dialysis patients use peritoneal dialysis, with a majority concentrated in some countries. To address these challenges, improved education will be required to improve education, increase investment in healthcare infrastructure, increase reimbursement policies and to further infections and reduce technological innovations that reduce costs, which leads to more virtuous and attractive option for patients worldwide.

Risks & Prospects in Peritoneal Dialysis Market

Major market occasions include increasing global phenomena of end-stage renewal disease (ESRD) and chronic kidney disease (CKD), inspired by an ageing population and increasing prevalence of diabetes and hypertension. The government's initiative and favourable reimbursement policies, especially in the US and Canada, are accelerating further adoption, while innovation is improving innovation treatment results in peritoneal dialysis solutions (such as advanced pH buffers and osmotic agents) and expanding the addressable patient pools.

Regionally, North America dominates the market due to its advanced healthcare infrastructure, high ESRD circulation and strong insurance coverage, with Americans accounting alone for a significant part of global dialysis patients. However, the Asia-Pacific region is expected to be the fastest-growing market, which is fuel to expand dialysis access by a large CKD patient base, rapid health service infrastructure development, increasing awareness and supporting government measures in countries such as China and India. Europe also remains a major market with strong adoption rates and established reimbursement systems. The combination of increasing disease burden, technological innovation, and expanding home-based care options offers sufficient opportunities for development and entry into the market worldwide.

Key Target Audience

Peritoneal dialysis (PD) market targets a diverse patient population, including individuals with end-stage renal disease (ESRD), especially diabetes, hypertension and cardiovascular comorbidities. They are the major demographics in elderly patients and rural or underdeveloped areas, as PD in selectors offers a home-based, low-resource-intensive option for haemodialysis. It is particularly beneficial in areas limited to modality dialysis centers, providing flexibility and a better quality of life for patients.

,,

,, ,,

Healthcare providers such as nephrologists, dialysis nurses and home care professionals are important stakeholders in PD markets. Adopting PDs and PD recommendations are affected by factors such as the patient's results, ease of use and health policies promoting home-based treatments. Like India's National Dialysis Program, by investing in government initiatives, infrastructure and training, the goal is to increase PD reach in rural areas, especially in rural areas. Such programmes not only expand the patient's base but also encourage health professionals to consider PDs as a viable treatment option, leading to an increase in the market.

Merger and acquisition

The peritoneal dialysis market has experienced remarkable merger and acquisition (M&A) activity in recent years, which reflects a strategic change towards innovation and patient-focused care. In August 2024, Baxter International Inc. announced the division of its kidney care segment for the Carlile Group, forcing a Venative, a standalone kidney care company. This step allows the Baxter to streamline its operation and focus on hospital solutions and connected care, which is the purpose of specialisation in advanced dialysis technologies.

Additionally, the launch of Mozarc Medical in April 2023 – a joint venture between Medtronic PLC and Davita Inc. – reflects the commitment to changing kidney health through patient-focused technology solutions. These strategic cooperations and partitions outlined the industry's attention on increasing home-based dialysis options and expanding global access, especially in emerging markets with increasing demand for accessible kidney care solutions.

>

Analyst Comment

The global peritoneal dialysis market is experiencing strong growth, with market evaluation from about 9.98 billion USD in 2025 increasing to USD 14.91 billion by 2032. This expansion is inspired by the increasing circulation of chronic kidney disease (CKD). Peritoneal dialysis solutions and technological progress in systems, with favourable government initiatives and reimbursement policies – especially in North America – are especially giving more fuel to the market. The Asia-Pacific is emerging as the fastest-growing sector, supported by expanding healthcare infrastructure and active government support in countries such as China and India.

- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Peritoneal Dialysis- Snapshot

- 2.2 Peritoneal Dialysis- Segment Snapshot

- 2.3 Peritoneal Dialysis- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Peritoneal Dialysis Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 CAPD

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 APD

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Peritoneal Dialysis Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Home health care

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Hospitals and Others

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

6: Peritoneal Dialysis Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Baxter International Inc.

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Fresenius Kabi AG

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Medtronic

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Utah Medical Products

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Inc.

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Glomeria Therapeutics

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Poly Medicure Ltd.

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Cook Medical Inc.

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 CardioMed Supplies

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Inc.

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Medical Components

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Inc.

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Other players

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the estimated market size of Peritoneal Dialysis in 2030?

+

-

Which type of Peritoneal Dialysis is widely popular?

+

-

What is the growth rate of Peritoneal Dialysis Market?

+

-

What are the latest trends influencing the Peritoneal Dialysis Market?

+

-

Who are the key players in the Peritoneal Dialysis Market?

+

-

How is the Peritoneal Dialysis } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Peritoneal Dialysis Market Study?

+

-

What geographic breakdown is available in Global Peritoneal Dialysis Market Study?

+

-

Which region holds the second position by market share in the Peritoneal Dialysis market?

+

-

How are the key players in the Peritoneal Dialysis market targeting growth in the future?

+

-

The peritoneal dialysis (PD) market is powered by several major factors. A primary driver is the increasing global prevalence of end-stage renal disease (ESRD), which is often the result of the increasing incidence of chronic conditions such as diabetes and high blood pressure. Since the number of patients requiring renal replacement therapy is increasing, the demand for effective dialysis solutions, a viable and often preferred option for many with PDs, is offered. Additionally, the population of growing agers worldwide is an important contributor, as older people are susceptible to kidney-related disorders and can prefer the low-disruptive nature of home-based PDs.

,Another important market driver is the increasing preference for home-based dialysis treatment. Peritoneal dialysis provides patients more flexibility, freedom and a better quality of life than in-centre haemodialysis, as it can be done in the comfort of their own homes. This change is further supported by technological progress in PD devices, such as more portable automated peritoneal dialysis (APD) cycles and remote monitoring systems, which increase home remedies and efficiency.