Global Nanocellulose Technology Market Size, Share & Trends Analysis Report, Forecast Period, 2024-2030

Report ID: MS-936 | Healthcare and Pharma | Last updated: May, 2025 | Formats*:

Nanocellulose technology markets include the global industry, which focuses on research, development, production and commercialisation of nanocellulose and related technologies. Nanocellulose is a durable, renewable nanomaterial that is derived from plant cellulose, which has exceptional properties such as a high strength-to-vision ratio, biodegradability, a large surface area and remarkable mechanical and thermal stability. The market contains various forms of nanocellulose, mainly cellulose nanocrystals (CNC), cellulose nanofibrils (CNF), and bacterial nanocellulose (BNC), each of which offers unique features and applications.

Market growth is inspired by the growing demand for durable and bio-based materials in a wide range of industries, including paper and packaging, composites, pharmaceuticals, biomedicals, electronics and food and beverage. Nanocellulose provides environmentally friendly options for petroleum-based products and is being adopted rapidly due to its better performance characteristics, such as increasing the strength and obstacle properties of paper and packaging, improving the mechanical properties of composites, and offering biocompatibility to medical applications.

Nanocellulose Technology Report Highlights

| Report Metrics | Details |

|---|---|

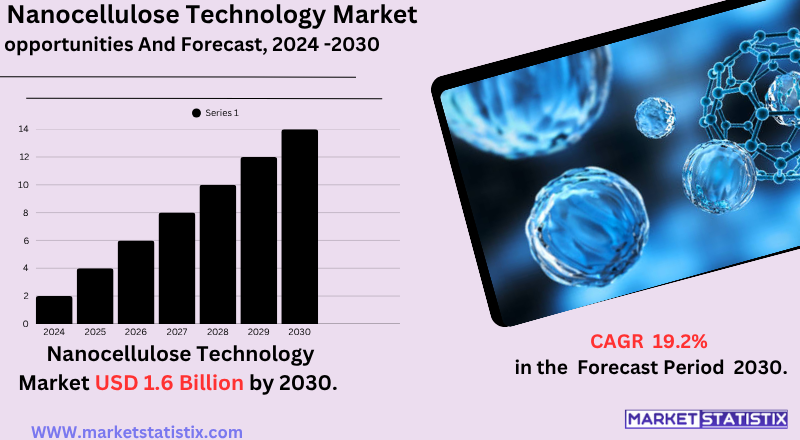

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 19.2% |

| Forecast Value (2030) | USD 1.6 Billion |

| By Product Type | Cellulose Nanocrystals, Cellulose Nanofibrils, Bacterial Nanocellulose |

| Key Market Players |

|

| By Region |

|

Nanocellulose Technology Market Trends

A major trend is to widely adopt nanocellulose as a permanent alternative to traditional petroleum-based products, especially in industries such as packaging, where it improves obstruction properties and biodegradability, and composites, where it contributes to light and high-strength materials such as automotive parts. This change has been motivated to promote environmentally friendly solutions by stringent government rules and create a favourable regulatory environment for nanocellulose, banning single-use plastic.

Researchers and manufacturers are actively developing to remove traditional production challenges such as enzymatic and green chemical methods, high costs and scalability. This innovation is expanding the range of nanocellulose types (such as cellulose nanocrystals and nanofibrils) and their functional properties, new and emerging applications in different fields such as biomedicine (e.g., wound healing, drug distribution), electronics (e.g., flexible displays) and even smart and flexible displays.

Nanocellulose Technology Market Leading Players

The key players profiled in the report are Kruger Inc., Fiberlean technologies, Oji Holdings Corporation, FPInnovations, GranBio, CelluComp Ltd, Celluforce INC, Borregard, Nippon Paper Industries, American Process Inc, Stora Enso, Blue Goose Refineries, Rise Innventia,, UPMGrowth Accelerators

The nanocellulose technology market is mainly inspired to increase global demand for durable and environmentally friendly materials. With increasing awareness about climate change and adverse effects of petroleum-based products, industries are actively looking for bio-based and biodegradable options. Nanocellulose, obtained from the Akshaya plant sources and keeping excellent properties such as high strength, low density and biodegradability, aligns with these stability goals in diverse areas such as packaging, motor vehicles, construction and textiles. Strict government regulations globally, especially on single-use plastics, expedite adopting nanocellulose as a viable and environmentally conscious material.

Beyond environmental views, technological progress in nanocellulose production and processing methods is greatly increasing the development of the market. Ongoing research and development efforts have led to more efficient, cost-effective and scalable manufacturing techniques, making nanocellulose a more commercially viable option. Its unique properties, such as high tensile strength, barrier capacity and biochemicals, are also expanding the scope of its application, especially in the drugs, biomedicals (e.g., wound dressing, drug distribution) and electronics industries.

Nanocellulose Technology Market Segmentation analysis

The Global Nanocellulose Technology is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Cellulose Nanocrystals, Cellulose Nanofibrils, Bacterial Nanocellulose . The Application segment categorizes the market based on its usage such as Composites, Paper and Pulp, Pharmaceuticals and Biomedical, Food and Beverages, Electronics. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The nanocellulose technology market has seen a moderate level of merger and acquisition (M&A) activity; strategic cooperation is often more prevalent than a lump sum acquisition. This reflects the early-to-middle phase of commercialisation for nanocellulose, where companies often focus on scaling production, developing specific applications and gaining partnerships to accelerate the market. Notable examples include traditional paper and pulp companies, who are the leading manufacturers of cellulose, investing in nanocellulose experts to diversify their portfolio and capitalise on growing demand for bio-based materials.

Recent M&A and strategic tricks in the market include companies such as Nippon Paper Industries, which acquired Allopak ASA to increase their paper-based packaging solutions, and Verhan KG has acquired a major manufacturer of Fibralen Technologies, Microfabricated Celluloses. These actions highlight a tendency where large content science companies are integrating nanocellulose capabilities to strengthen their offerings in permanent packaging, composites and other high-protest applications. These deals are often focused on vertical integration, access to proprietary production technologies and reaching the market in new inter-use industries.

Challenges In Nanocellulose Technology Market

Nanocellulose technology market faces significant challenges that obstruct its broader commercial adoption. The major ones of these are high production costs and limited scalability, which make it difficult to compete with traditional materials in terms of price and availability for nanocellulose. The manufacturing process requires advanced machinery, special technical expertise and adequate initial investment, which contribute to all high costs and restrict the ability to increase production efficiently.

Regulatory and security concerns further disrupted market growth. The legal framework around nanocellulose remains unclear and inconsistent in areas, resulting in uncertainty and compliance and safety requirements for manufacturers and end-users. There are also unresolved issues related to the characterisation of nanocellulose, as current methods are often slow, indirect, and do not adapt to industrial needs, making quality control and process difficult. These factors, combined with the requirement of disruption in the supply chain and the need for harmonious standards, create obstacles for innovation and slow down the speed of market expansion despite the promising properties and stability benefits of the material.

Risks & Prospects in Nanocellulose Technology Market

The major market opportunities are grown by the unique properties of nanocellulose – high power-to-wisdom ratio, biodegradability and large surface areas – which make it attractive to a wide range of industries. Major growth drivers include permanent packaging, light motor vehicle components, biomedical products and increasing demand for advanced electronics. Innovations in production methods, such as enzymatic treatment and cold plasma processing, reduced costs and expanded potential applications.

Regionally, Europe is expected to dominate the European market due to significant investment in R&D, strong demand for permanent paper and pulp applications, and strong government and commercial sector support. However, countries such as Asia-Pacific China and India are rapidly emerging as high-development areas operated by industrialisation, increasing use of motor vehicles and electronics, and expanding manufacturing capabilities. Other areas, including North America and Australia-New Zealand, are also experiencing significant growth, supported by regulatory changes in favour of green content and increased consumer awareness about environmental stability. The global expansion, combined with sector-specific innovations, keeps nanocellulose technology as a major enabler in infection for green industrial solutions.

Key Target Audience

The major target audiences for the nanocellulose technology market are incredibly diverse, spreading in many industrial areas that are rapidly sustainable, high-demonstration materials. Primary segments include paper and packaging industries, where nanocellulose increases the power, barrier properties and biodegradability of products such as food packaging and paperboard. Composite and automotive industries are also important goals, which use nanocellulose to develop lighter, stronger and more fuel-efficient materials for vehicles and other structural applications, which are motivated by the need for weight loss and better performance.

,, ,,

Beyond these large-volume applications, other important goals include the pharmaceutical and biomedical sectors in the audience, interested in nanocellulose for drug delivery systems, wound dressing, tissue engineering and medical implants, which are due to its biocompatibility and non-toxicity. The electronics industry examines its use in flexible displays, sensors and other advanced electronic components. Additionally, the food and beverage industry use nanocellulose as a stabiliser, thickener and passion, while paints and coatings and individual care fields also represent growing opportunities, which are motivated by better product performance and demand for environmentally friendly yogas.

,,

Merger and acquisition

The nanocellulose technology market has seen a moderate level of merger and acquisition (M&A) activity; strategic cooperation is often more prevalent than a lump sum acquisition. This reflects the early-to-middle phase of commercialisation for nanocellulose, where companies often focus on scaling production, developing specific applications and gaining partnerships to accelerate the market. Notable examples include traditional paper and pulp companies, who are the leading manufacturers of cellulose, investing in nanocellulose experts to diversify their portfolio and capitalise on growing demand for bio-based materials.

Recent M&A and strategic tricks in the market include companies such as Nippon Paper Industries, which acquired Allopak ASA to increase their paper-based packaging solutions, and Verhan KG has acquired a major manufacturer of Fibralen Technologies, Microfabricated Celluloses. These actions highlight a tendency where large content science companies are integrating nanocellulose capabilities to strengthen their offerings in permanent packaging, composites and other high-protest applications. These deals are often focused on vertical integration, access to proprietary production technologies and reaching the market in new inter-use industries.

>Analyst Comment

The global nanocellulose technology market is experiencing rapid growth, with a strong CAGR in 2025, with approximate estimates from USD 3 billion and USD 3 billion from USD 3 billion and USD from 2034-2035. This boom has increased by increasing demand for sustainable, biodegradable materials in diverse industries, including packaging, healthcare, electronics, automotive and textiles. The plant provides exceptional properties such as nanocellulose, a high-strength-to-vision ratio, biodegradability, and a large surface area, which makes it an attractive option for petroleum-based products and synthetic polymers.

- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Nanocellulose Technology- Snapshot

- 2.2 Nanocellulose Technology- Segment Snapshot

- 2.3 Nanocellulose Technology- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Nanocellulose Technology Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Cellulose Nanofibrils

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Cellulose Nanocrystals

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Bacterial Nanocellulose

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

5: Nanocellulose Technology Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Composites

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Paper and Pulp

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Food and Beverages

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Pharmaceuticals and Biomedical

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

- 5.6 Electronics

- 5.6.1 Key market trends, factors driving growth, and opportunities

- 5.6.2 Market size and forecast, by region

- 5.6.3 Market share analysis by country

6: Nanocellulose Technology Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Borregard

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Fiberlean technologies

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Celluforce INC

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Nippon Paper Industries

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Rise Innventia

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 Stora Enso

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 American Process Inc

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 FPInnovations

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Oji Holdings Corporation

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Blue Goose Refineries

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 GranBio

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 CelluComp Ltd

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 Kruger Inc.

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 UPM

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the estimated market size of Nanocellulose Technology in 2030?

+

-

Which type of Nanocellulose Technology is widely popular?

+

-

What is the growth rate of Nanocellulose Technology Market?

+

-

What are the latest trends influencing the Nanocellulose Technology Market?

+

-

Who are the key players in the Nanocellulose Technology Market?

+

-

How is the Nanocellulose Technology } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Nanocellulose Technology Market Study?

+

-

What geographic breakdown is available in Global Nanocellulose Technology Market Study?

+

-

Which region holds the second position by market share in the Nanocellulose Technology market?

+

-

How are the key players in the Nanocellulose Technology market targeting growth in the future?

+

-

The nanocellulose technology market is mainly inspired to increase global demand for durable and environmentally friendly materials. With increasing awareness about climate change and adverse effects of petroleum-based products, industries are actively looking for bio-based and biodegradable options. Nanocellulose, obtained from the Akshaya plant sources and keeping excellent properties such as high strength, low density and biodegradability, aligns with these stability goals in diverse areas such as packaging, motor vehicles, construction and textiles. Strict government regulations globally, especially on single-use plastics, expedite adopting nanocellulose as a viable and environmentally conscious material.

,,Beyond environmental views, technological progress in nanocellulose production and processing methods is greatly increasing the development of the market. Ongoing research and development efforts have led to more efficient, cost-effective and scalable manufacturing techniques, making nanocellulose a more commercially viable option. Its unique properties, such as high tensile strength, barrier capacity and biochemicals, are also expanding the scope of its application, especially in the drugs, biomedicals (e.g., wound dressing, drug distribution) and electronics industries.