Global Medical Trolley Market - Industry Dynamics, Market Size, And Opportunity Forecast To 2030

Report ID: MS-933 | Healthcare and Pharma | Last updated: May, 2025 | Formats*:

The medical trolley market refers to the global industry that produces, distributes, and sells customized carts and trolleys for use in medical environments. Such necessary equipment is utilised to transport medical supplies, drugs, diagnostic equipment, and medical equipment within clinics, hospitals, long-term care facilities, and other medical facilities efficiently. The market offers numerous trolley variations, including emergency trolleys (crash carts), anaesthesia trolleys, medication trolleys, procedure trolleys, and isolation trolleys, all designed for specific medical applications and workflows.

The major drivers for this market are the increasing expenditure on healthcare across the globe, the growing number of surgical procedures, and an increased focus on infection control and patient safety. The demand for point-of-care solutions and the need for efficient medical supply management also significantly contribute to the growth of the medical trolley market.

Medical Trolley Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

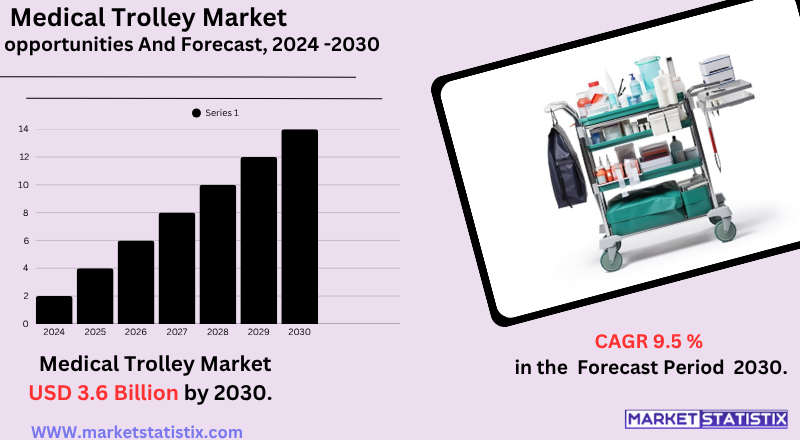

| Growth Rate | CAGR of 9.5% |

| Forecast Value (2030) | USD 3.6 Billion |

| By Product Type | Powered medical trolleys, Integrated medical trolleys |

| Key Market Players |

|

| By Region |

|

Medical Trolley Market Trends

The medical trolley market is now experiencing significant trends fuelled by the changing healthcare landscape. One key trend is the increasing presence of advanced technology, such as electronic locking systems for improved security, ergonomic design to prevent fatigue of healthcare professionals, and the utilisation of antimicrobial materials to enhance infection control. In addition, there's an increasing need for power supply-toting trolleys for medical devices and electronic health record (EHR) connectivity, making them mobile workstations. Telemedicine expansion and the need for portable equipment for virtual consultation purposes also drive demand for high-tech medical trolleys.

Customisation and modularity are another trend where it's trending towards focusing on customisation and modularity. Healthcare environments need flexible solutions that can be easily programmed to address various departments and workflows. Manufacturers are answering back with customizable and modular trolley designs that can be configured easily for particular uses such as medication dispensing, emergency response, or carrying specialised equipment. This trend, combined with the growing focus on enhancing patient safety and nursing efficiency, is driving innovation in trolley design, producing more versatile, durable, and easy-to-use products.

Medical Trolley Market Leading Players

The key players profiled in the report are Bytec, Villard, Athena, JACO, Enovate, Capsa Solutions, CompuCaddy, Scott-Clark, Stanley, Parity Medical, ITD, Rubbermaid, InterMetro(Emerson), Curarket forecast,Growth Accelerators

The medical trolley industry is witnessing tremendous growth due to a host of factors. Most importantly, rising global healthcare spending and widening healthcare infrastructure are driving demand. With governments and private players investing increasingly in setting up and upgrading hospitals, clinics, and other healthcare facilities, demand for ancillary equipment such as medical trolleys to efficiently manage and transport supplies follows naturally. Also, the increasing number of surgeries and emergency situations globally further demands a strong supply of speciality trolleys, like crash carts and anaesthesia carts, in order to provide immediate and effective patient care.

In addition, technology is coming into play. Contemporary medical trolleys are embracing aspects such as electronic lock systems, ergonomic controls to minimise stress on medical staff, onboard power supplies for medical equipment, and even compatibility with electronic health records (EHRs), all with the aim of increased efficiency and patient care.

Medical Trolley Market Segmentation analysis

The Global Medical Trolley is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Powered medical trolleys, Integrated medical trolleys . The Application segment categorizes the market based on its usage such as Nurses Use, Doctors Use, Others. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The medical trolley market is characterised by competitive intensity with the coexistence of both global leaders and many regional players competing for market share via product development, strategic collaborations, and pricing competition. Major global producers such as Ergotron, Capsa Solutions, Enovate Medical, InterMetro (Emerson), and Rubbermaid are well-established, typically controlling North American and European markets through their superior R&D capabilities and massive distribution channels. These big players specialise in creating technologically superior trolleys with aspects like built-in electronic systems, ergonomic layouts, and infection-control characteristics to address the changing demands of contemporary healthcare facilities.

Outside of these market leaders, the scene is also dominated by a strong base of local as well as specialised producers, especially in the Asia-Pacific region. These local competitors tend to battle on price competitiveness, customisation capabilities, and close working relationships with regional healthcare providers. The market is also experiencing specialisation, with companies concentrating on individual types of trolleys, such as emergency carts, medication carts, or procedure carts, and also creating solutions for niche uses like telehealth and mobile computing. This competitive energy fosters ongoing innovation and presents the healthcare facilities across the globe with a wide variety of products.

Challenges In Medical Trolley Market

The market for medical trolleys, though witnessing strong growth owing to increasing healthcare infrastructure and advancing technology, is challenged by some major issues. The most prominent challenge lies in the cost of expensive high-end trolleys, particularly those with features such as automation, AI integration, and RFID. These high costs are likely to be out of reach for smaller healthcare units and providers in emerging economies, thereby restricting large-scale adoption. In addition, repeated maintenance costs, regular cleaning and disinfection needs, and the complexity of adapting new technologies to current hospital systems also contribute to operational burdens.

Another significant challenge is regulatory compliance and standardisation of the product since medical trolleys have to adhere to high levels of safety, quality, and infection control standards that differ from region to region. This not only drives up production costs but also makes it difficult for manufacturers to enter the market. The requirement for training staff to utilise technologically sophisticated trolleys, limited spaces in smaller facilities, and the requirement for customisation to accommodate varied medical environments further make manufacturing and supply chains challenging.

Risks & Prospects in Medical Trolley Market

Major market opportunities are the expanding demand for effective inventory management, optimised clinical workflows, and integrating digital health solutions such as electronic medical records (EMRs) and electronic health records (EHRs). The demand for speciality trolleys—e.g., anaesthesia, crash, medication, and procedure carts—is growing as clinics and hospitals aim to enhance patient care, safety, and operational efficiency. In addition, powered or integrated trolleys and ergonomic designs are becoming increasingly popular, especially with healthcare professionals looking to mitigate staff fatigue and enhance productivity.

At the regional level, North America dominates the market because of its sophisticated healthcare infrastructure, dense population of major players, and early embracement of cutting-edge medical technologies, with the United States accounting for approximately 37% of the global share. Europe's developed market focuses on ergonomics and strict compliance with regulations, whereas the fastest growth is expected in the Asia Pacific region, driven by growing healthcare investments, increasing disposable incomes, and a fast-growing ageing population—particularly in China and India. Latin America and the Middle East & Africa are also likely to experience consistent and high growth as healthcare modernisation and awareness of effective care solutions continue to increase in these markets.

Key Target Audience

,, ,

The primary target groups for the medical trolley market are mainly hospitals, clinics, ambulatory surgical centers, and healthcare facilities. Medical trolleys are needed by these institutions in order to have efficient storage, transport, and easy access to medical equipment and supplies. Demand is spurred by the necessity for workflow efficiency, improved patient care, and infection control, particularly within hectic settings like emergency wards and surgery rooms.

,Besides, the market also addresses healthcare procurement managers, hospital administrators, and medical device distributors who make purchasing decisions. Increasing adoption of technologically advanced and customizable trolleys is also attractive to facility planners and IT integration experts in healthcare organizations. Healthcare infrastructure growth, an ageing population, and rising surgical procedures around the world further increase the target audience base for medical trolley solutions.

Merger and acquisition

The medical trolley industry is undergoing substantial change, with advancements in technology and strategic mergers and acquisitions (M&A) at the forefront. Major players are shifting their emphasis toward the integration of digital health solutions and innovative product development to address the changing demands of healthcare organizations. For example, Advantech supplemented its product lineup with the AMiS-30EP pole cart, reflecting the sector's emphasis on innovation and customisation possibilities. In addition, the market is seeing a significant trend towards special-purpose solutions intended for particular medical applications and departments, especially surgical and emergency care departments.

Strategic M&A moves are becoming very important in determining the market landscape. Stryker Corporation, among other firms, has been aggressively buying companies to enhance their products and increase their international presence. Stryker finalised the acquisition of French joint replacement company SERF SAS in March 2024, growing stronger in the European market. Such a move allows companies to gain access to new technology, penetrate new markets, and improve their competitive edge.

>Analyst Comment

The worldwide market for medical trolleys is growing vigorously, reaching USD 1.6 billion in 2024 and likely to grow to USD 3.6 billion in 2034. This growth is caused by increased investment in healthcare facilities, the rising rate of chronic diseases, an ageing population, and technological innovation in trolley development—i.e., incorporated workstations, medication dispensing units, and antimicrobial coatings. Medical trolleys are essential to enhancing workflow efficiency, organisation, and infection control in the hospital and clinic setting and thus are unavoidable in contemporary healthcare provision.

- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Medical Trolley- Snapshot

- 2.2 Medical Trolley- Segment Snapshot

- 2.3 Medical Trolley- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Medical Trolley Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Powered medical trolleys

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Integrated medical trolleys

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Medical Trolley Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Doctors Use

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Nurses Use

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Others

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Medical Trolley Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 Capsa Solutions

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Enovate

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 InterMetro(Emerson)

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Rubbermaid

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Parity Medical

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 ITD

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 JACO

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Stanley

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Villard

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Scott-Clark

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Athena

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Bytec

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 CompuCaddy

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 Curarket forecast

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

- 8.15

- 8.15.1 Company Overview

- 8.15.2 Key Executives

- 8.15.3 Company snapshot

- 8.15.4 Active Business Divisions

- 8.15.5 Product portfolio

- 8.15.6 Business performance

- 8.15.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Medical Trolley in 2030?

+

-

Which application type is expected to remain the largest segment in the Global Medical Trolley market?

+

-

How big is the Global Medical Trolley market?

+

-

How do regulatory policies impact the Medical Trolley Market?

+

-

What major players in Medical Trolley Market?

+

-

What applications are categorized in the Medical Trolley market study?

+

-

Which product types are examined in the Medical Trolley Market Study?

+

-

Which regions are expected to show the fastest growth in the Medical Trolley market?

+

-

Which application holds the second-highest market share in the Medical Trolley market?

+

-

What are the major growth drivers in the Medical Trolley market?

+

-

The medical trolley industry is witnessing tremendous growth due to a host of factors. Most importantly, rising global healthcare spending and widening healthcare infrastructure are driving demand. With governments and private players investing increasingly in setting up and upgrading hospitals, clinics, and other healthcare facilities, demand for ancillary equipment such as medical trolleys to efficiently manage and transport supplies follows naturally. Also, the increasing number of surgeries and emergency situations globally further demands a strong supply of speciality trolleys, like crash carts and anaesthesia carts, in order to provide immediate and effective patient care.

In addition, technology is coming into play. Contemporary medical trolleys are embracing aspects such as electronic lock systems, ergonomic controls to minimise stress on medical staff, onboard power supplies for medical equipment, and even compatibility with electronic health records (EHRs), all with the aim of increased efficiency and patient care.