Global Grid Energy Storage Market Trends and Forecast to 2030

Report ID: MS-671 | Energy and Natural Resources | Last updated: Apr, 2025 | Formats*:

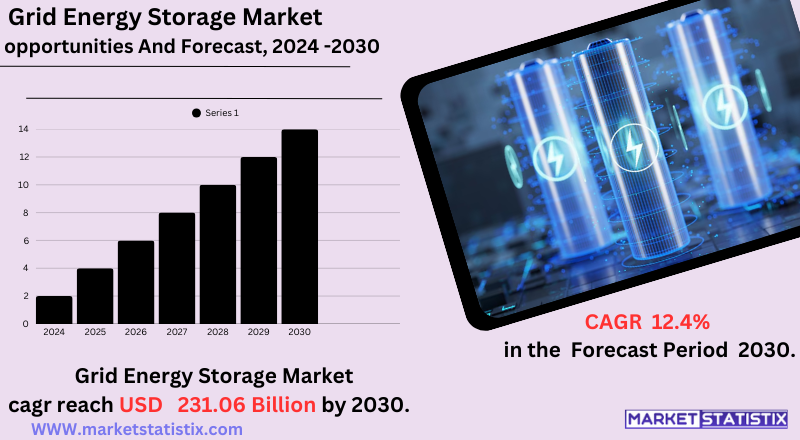

Grid Energy Storage Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

| Growth Rate | CAGR of 12.4% |

| Forecast Value (2030) | USD 231.06 Billion |

| By Product Type | Pumped Hydro Storage, Lithium-ion batteries, Others |

| Key Market Players |

|

| By Region |

|

Grid Energy Storage Market Trends

The grid energy storage market is ramping up in terms of deployment of battery energy storage system (BESS) technologies elicited by falling prices and advances in lithium-ion batteries. In addition to this, there is an increasing trend toward using renewable energy sources that require grid stabilisation and flexible energy management. Along with it, there are also advancements made toward long-duration energy storage (LDES) technologies like flow batteries and pumped hydro systems for future grid reliability during long periods of low renewable energy generation. In addition, policy support and regulatory frameworks are quite instrumental in changing trends within markets. Although governments worldwide apply a stimulus and mandates for grid energy storage, they do not wish to omit funds for achieving a decarbonising goal. This has also led to increasing co-operations between energy storage providers, renewable energy developers, and utilities that would come up with new and better business models and integrated energy solutionsGrid Energy Storage Market Leading Players

The key players profiled in the report are Tesla (U.S.), Hitachi Energy (Japan), Panasonic Corporation (Japan), VRB Energy (Canada), LG Energy Solution (South Korea), Siemens (Germany), NGK Insulators (Japan), BYD (China), CATL (China), ABB (Switzerland), GE Vernova (U.S.), Honeywell (U.S.), Toshiba Corporation (Japan), Samsung SDI (South Korea), Mitsubishi Heavy Industries, Ltd. (Japan)Growth Accelerators

A primary impetus is the growing integration of variable renewable energy resources, such as solar and wind, into electricity grids. Such resources require energy storage to offset their intermittency and stabilise the grid. Furthermore, the heightened focus on grid modernisation and resilience, stemming from the necessity to avert power outages and improve reliability, drives demand for such advanced storage solutions. Also contributing to the viability of grid-scale storage are the drastically falling costs, especially of lithium-ion battery technologies. Cost reduction and advancements in the others' storage technologies, like flow batteries and compressed air energy storage, create a wider range of storage solutions that can be available and competitively marketed. These include the need for peak shaving, frequency regulation, and ancillary services that could enhance the grid's efficiency, which is another pulling factor for large-scale energy storage investments across the globe.Grid Energy Storage Market Segmentation analysis

The Global Grid Energy Storage is segmented by Type, Application, and Region. By Type, the market is divided into Distributed Pumped Hydro Storage, Lithium-ion batteries, Others . The Application segment categorizes the market based on its usage such as Commercial & Industrial, Residential, Others. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The grid energy storage market is subject to interesting competitive rivalry created between its large established energy companies and new technology innovators. They are into serious races toward advanced development and deployment of innovative storage solutions focused mostly on emerging battery technologies, system-efficient performance, and cost reduction. This driver has brought about remarkable progress in lithium-ion batteries, flow batteries, and other storage technologies along with creating a more diverse and robust market. In addition, regional dynamics are significant, with the three contenders of the Asia-Pacific region, North America, and Europe presenting themselves differently in terms of regulations and market drivers. Therefore, the definition of this competitive landscape is by technological innovations, strategic collaborative approaches, and market dynamics at a regional level.Challenges In Grid Energy Storage Market

A few obstacles in energy storage associated with the grid reflect on its scalability and efficiency. Some of them include dependency on critical minerals, lithium-cobalt-nickel-based, for battery production. Soaring costs of these mineral imports, disruption of mobility due to geopolitical strife and competition offsets with EV markets make it hard to keep costs down and broaden deployment installation horizons. This long-term permitting and interconnection delays/uncertainties relating to regulations hamper timely implementation of storage projects in various domains. Basically, they translate the factor risk in investments and majorly slow down ambitious decarbonisation targets. The other challenge faced in energy storage is its integration with renewable energy sources. Usually, renewable generation varies depending on weather conditions, and this mismatch between supply and demand needs to be forecast well and optimised storage solutions installed to keep the grid supply in balance. Technological innovations using more than one storage method and new regulations will finally assist in unlocking all potential that energy storage can offer in grids.Risks & Prospects in Grid Energy Storage Market

Advanced battery technologies present great opportunities. Lithium-ion systems are getting increasingly economical and more competent. They flourish within the new business framework of Energy Storage-as-a-Service (ESaaS) and capacity contracts. That has widened the available market for flexible arrangements for peak load management and the integration of renewable power. On the other hand, North America remains the best-case scenario for corresponding promising political, technological, and investment fortunes in renewable energy infrastructure. An already established grid in the region facilitates the seamless incorporation of storage facilities to counter risks such as a "duck curve", ensuring stability in grids even with fluctuating demand. This also makes Europe a key market as a result of its aggressive climate goals related to decarbonised renewable energy build-out. All of that highlights different growth drivers in different parts of the global markets so that grid storage energy becomes an important factor or enabler in the transition to sustainable energy systems.Key Target Audience

The grid energy storage market is primarily targeting utility companies, grid operators, and energy providers. Utilities use the storage systems to store excess energy generated from renewables like wind and solar, in turn providing a steady supply during peak demand times or low renewable generation times. The grid operators benefit from these systems when managing peak load, frequency regulation, voltage support, and procuring ancillary services that increase grid reliability and efficiency. Energy providers utilise grid storage for better integration with renewables, operation optimisation, capital expenditure deferral, and with a view to increasing customer reliability., Governments and policymakers constitute another major audience toward whom energy storage systems in the grid are marketed due to providing incentives, subsidies, and mandates for renewable energy integration. Grid storage systems are, moreover, relied upon by emerging markets, industries transitioning to clean energy, and electric vehicle (EV) charging infrastructure for growing energy demands. Oligopolies commercially invest in advancing battery technologies and AI-optimised energy to extend the market and conquer challenges like intermittency and cost.Merger and acquisition

Recent merger and acquisition activity in the grid energy storage market continues with a trend of strategic consolidation and technological advancement. In 2022, Powin Energy acquired EKS Energy to improve energy storage through advanced power conversion technologies. This trend indicates the industry's focus on optimising energy storage systems for grid performance and renewable energy integration. Corporate funding in energy storage grew massively in 2024, to $19.9 billion, with M&A activity being a very important driver of this growth. The ever-growing demand for energy storage owing to needs for renewable energy integration and grid resilience continues to attract M&A deals and investors. >Analyst Comment

Substantial growth is evident in the grid energy storage market, due in large part to the global transition toward integrating renewables and thereby enhancing grid stability. Owing to the declining costs and enhanced performance of battery energy storage systems (BESS), market analysis points to a surge in investment in these systems. This is coupled with government support and incentive schemes aimed at modernizing grid infrastructure and promoting clean energy solutions. Thus, the market has become competitive, with major players engaging in technological innovations and strategic alliances to increase their market share.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Grid Energy Storage- Snapshot

- 2.2 Grid Energy Storage- Segment Snapshot

- 2.3 Grid Energy Storage- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Grid Energy Storage Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Pumped Hydro Storage

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Lithium-ion batteries

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Others

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

5: Grid Energy Storage Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Residential

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Commercial & Industrial

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Others

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Grid Energy Storage Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 BYD (China)

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Samsung SDI (South Korea)

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Tesla (U.S.)

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Panasonic Corporation (Japan)

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 LG Energy Solution (South Korea)

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 GE Vernova (U.S.)

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 ABB (Switzerland)

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 Hitachi Energy (Japan)

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Honeywell (U.S.)

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Siemens (Germany)

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Toshiba Corporation (Japan)

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 CATL (China)

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

- 8.13 NGK Insulators (Japan)

- 8.13.1 Company Overview

- 8.13.2 Key Executives

- 8.13.3 Company snapshot

- 8.13.4 Active Business Divisions

- 8.13.5 Product portfolio

- 8.13.6 Business performance

- 8.13.7 Major Strategic Initiatives and Developments

- 8.14 VRB Energy (Canada)

- 8.14.1 Company Overview

- 8.14.2 Key Executives

- 8.14.3 Company snapshot

- 8.14.4 Active Business Divisions

- 8.14.5 Product portfolio

- 8.14.6 Business performance

- 8.14.7 Major Strategic Initiatives and Developments

- 8.15 Mitsubishi Heavy Industries

- 8.15.1 Company Overview

- 8.15.2 Key Executives

- 8.15.3 Company snapshot

- 8.15.4 Active Business Divisions

- 8.15.5 Product portfolio

- 8.15.6 Business performance

- 8.15.7 Major Strategic Initiatives and Developments

- 8.16 Ltd. (Japan)

- 8.16.1 Company Overview

- 8.16.2 Key Executives

- 8.16.3 Company snapshot

- 8.16.4 Active Business Divisions

- 8.16.5 Product portfolio

- 8.16.6 Business performance

- 8.16.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Grid Energy Storage in 2030?

+

-

Which application type is expected to remain the largest segment in the Global Grid Energy Storage market?

+

-

How big is the Global Grid Energy Storage market?

+

-

How do regulatory policies impact the Grid Energy Storage Market?

+

-

What major players in Grid Energy Storage Market?

+

-

What applications are categorized in the Grid Energy Storage market study?

+

-

Which product types are examined in the Grid Energy Storage Market Study?

+

-

Which regions are expected to show the fastest growth in the Grid Energy Storage market?

+

-

Which application holds the second-highest market share in the Grid Energy Storage market?

+

-

What are the major growth drivers in the Grid Energy Storage market?

+

-