Global Dry Electrode Technology Market – Industry Trends and Forecast to 2030

Report ID: MS-2076 | Electronics and Semiconductors | Last updated: Dec, 2024 | Formats*:

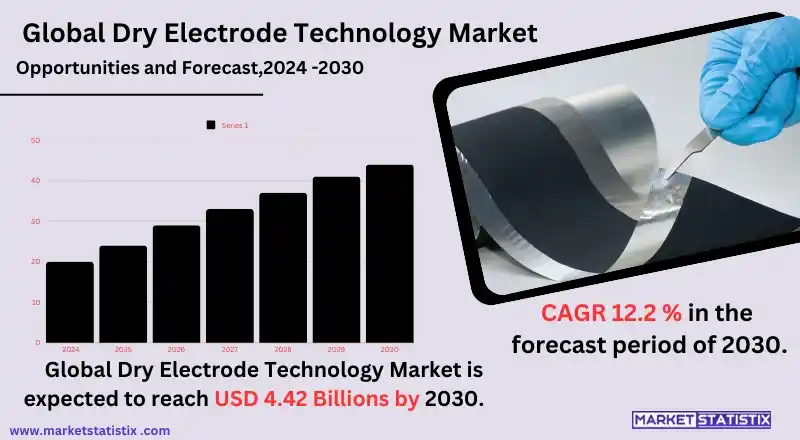

Dry Electrode Technology Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2023 |

| Growth Rate | CAGR of 12.2% |

| Forecast Value (2030) | USD 4.42 billion |

| By Product Type | General Dry Electrode Technology, Activated Dry Electrode Technology |

| Key Market Players |

|

| By Region |

|

Dry Electrode Technology Market Trends

The market for dry electrode technologies has been expanding rapidly owing to the increased need for energy-efficient and affordable energy storage systems, more so when it comes to electric vehicles (EVs) and renewable energy resources. One of the most notable trends is the advancement in technologies and materials that have enhancement applications in batteries. Manufacturers are also improving on the energy density, charging rate, and overall efficiency of dry electrodes in a bid to beat the conventional wet-based electrode technologies. One more trend that is worth mentioning is the increasing corporate investments in scaling up dry electrode technology for commercial use. This intergrowing sector involves battery-producing companies, material engineering companies, and research centres in order to fully utilise this technology commercially sooner rather than later. Furthermore, with the rise of the global electric vehicle market, an efficient high-performance battery is quite essential; hence, dry electrode technology is mostly at the forefront since the companies are employing this technology so as to enhance sustainability and cut down on production costs.Dry Electrode Technology Market Leading Players

The key players profiled in the report are AM Batteries, Maxwell Technologies, Fraunhofer IWS, LiCAP Technologies, Nano Dimension, Nanotech, NanoSonic, NanoSpectra, Shenzhen Tsingyan Electronic Technology Co., Ltd., KionixGrowth Accelerators

One of the primary market growth factors for the dry electrode technology market is the increasing need for efficient and less expensive energy storage systems, more so in the electric vehicle (EV) and renewable energy markets. As more manufacturing companies are focused on producing more and more EVs, which comes with the demand of building large energy storage systems, there is a need to improve battery capability while minimising the cost of its production. Dry electrode technology has other benefits, such as a decrease in fabrication time and material costs and the avoidance of harmful solvents, which makes it easier for its users to respond to such trends. Another point to note is that concern for the environment is growing quickly. In addition, it contributes to the eco-friendly manufacturing process as there are no toxic substances used and it is less energy intensive. The technology for dry electrodes has been on the rise in batteries as more and more policies and strategies are more focused on the minimisation of carbon emissions into the atmosphere and greener ways of producing batteries. This is in addition to material technology inventions and the quest for new battery types, which fuels the overall market expansion.Dry Electrode Technology Market Segmentation analysis

The Global Dry Electrode Technology is segmented by Type, Application, and Region. By Type, the market is divided into Distributed General Dry Electrode Technology, Activated Dry Electrode Technology . The Application segment categorizes the market based on its usage such as Capacitor, Lithium-ion Batteries, Sodium-ion Batteries, Other Battery Types. Geographically, the market is assessed across key Regions like North America(United States, Canada, Mexico), South America(Brazil, Argentina, Chile, Rest of South America), Europe(Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific(China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA(Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

When looking at the competition in the market for dry electrode technology, we found that companies like Tesla, LG Chem, Maxell Holdings, and Sakuu have been investing a lot in R&D with the aim of inventing and improving their manufacturing processes. Companies have also adopted dry electrode methods in a bid to increase energy density and cycle life in the batteries, which are very important factors with regard to the performance of electric vehicles. The market has a combination of big players and young companies that are experimenting on new uses of dry electrode technology in areas such as consumer electronics and renewable energy storage.Challenges In Dry Electrode Technology Market

The normal performance and scalability of production is one of the greatest hurdles in the dry electrode technology industry. The dry electrode process can have difficulties with processing active materials onto the conductor substrate, forming a uniform coating and adhesion, which affects efficiency and durability of the battery. The absence of liquid electrolytes introduces other drawbacks in terms of achieving an optimal interface between the electrode and the electrolyte, which in turn affects the electrochemical performance and energy density of the batteries. Coupled with this is the lack of advanced R&D necessary to enhance the technology and address the existing challenges. Dry electrodes can lower costs of production and minimise environmental impact, but even so, they are still quite recent and need some more modifications for them to compete with the performance of conventional wet electrode systems.Risks & Prospects in Dry Electrode Technology Market

The market for dry electrode technology has great prospects within the electric vehicles (EVs) sector, given that there is an increasing need for high-performing but affordable batteries. Since dry electrodes are designed to improve the efficiency of batteries and cut down on their production costs, they are aimed at addressing the high demand for cost-effective and environmentally friendly batteries for electric vehicles. The technology appeals to both consumers and manufacturers, who are environmentally inclined, because it is able to do away with toxic substances in the production processes of batteries, thus reducing the negative effects of battery production. There is also another opportunity in the improvement of consumer electronics and portable equipment as the need for lighter and longer-lasting batteries increases. With energy-hungry devices such as smart phones, laptops, and wearables, it will dry electrode technology mechanisms that will prolong working hours without having to increase the number of times charging is done. In addition, as further research is embarked upon in the fields of material science and production techniques, the technology in potential has room for improvement in terms of energy density and efficiency. This makes dry electrode technology an important component of the energy storage sector, making its demand grow in various fields.Key Target Audience

The primary target audience in the dry electrode technology market is focused ionically on the manufacturers of energy storage devices, for instance, battery makers, especially those who are into lithium as well as sodium-ion batteries. This is because there has been a need to find more efficient, cheaper, and eco-friendly ways of doing things. Industries depending on electric vehicles (EVs) and providing renewable energy storage systems are the other notable users of the dry electrode technology, where the quest is for innovations that enhance battery performance at a lower cost and higher mass-production scalability. Researching and supplying raw materials for the existing and new plants is another important target audience.,, This category includes all those who are concentrating on the development of relevant technologies for battery improvement. These people search for new materials and production techniques but also work on issues pertaining to how to change battery materials to make them more powerful, longer-lasting, and more environmentally friendly. They are instrumental in promoting the use of dry electrode technology in different applications such as consumer electronics, electric mobility, and large-scale battery applications since all these industries attune to the ever-growing need for portable power supply across the globe.Merger and acquisition

In the presently existing dry electrode technology market, various strategic alliances, mergers, and acquisitions have taken place in order to increase the scope of market penetration and improve the capacity of production. Additionally, on 17 November 2023, Dürr Group completed the acquisition of Ingecal, a French mechanical engineering firm. With this acquisition, Dürr aims to provide advanced machines capable of shot wet and dry coating processes; the device is necessary in the manufacture of battery electrodes. Such strategic collaborations with companies such as LiCAP Technologies also help fortify Dürr’s footing in the dry coating segment, as both companies venture into commercialisation of the innovative Activated Dry Electrode® technology. This approach will in turn improve the range of products and services from Dürr in the electromobility sector, which is characterised by the need for production technologies that are ‘green’ for battery manufacturing. Another noteworthy acquisition in the segment was performed by **Enerpoly**, which in July 2024 purchased Nilar’s cell production and pack assembly lines. By this acquisition, Enerpoly is set to adopt Nilar’s advanced dry electrode technology within its zinc-ion battery production processes. The company will apply this technology to trim its processes and expenditures and address the market’s demand for eco-friendly energy storage systems. These proactive stances are indicative of an overall structure in the sector where players are trying to reinvent and advance joint competition through M&As and technology, i.e., the global battery manufacturing competition.- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Dry Electrode Technology- Snapshot

- 2.2 Dry Electrode Technology- Segment Snapshot

- 2.3 Dry Electrode Technology- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Dry Electrode Technology Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 General Dry Electrode Technology

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 Activated Dry Electrode Technology

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

5: Dry Electrode Technology Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Capacitor

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Lithium-ion Batteries

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Sodium-ion Batteries

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

- 5.5 Other Battery Types

- 5.5.1 Key market trends, factors driving growth, and opportunities

- 5.5.2 Market size and forecast, by region

- 5.5.3 Market share analysis by country

6: Dry Electrode Technology Market by End-User

- 6.1 Overview

- 6.1.1 Market size and forecast

- 6.2 Automotive

- 6.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.2 Market size and forecast, by region

- 6.2.3 Market share analysis by country

- 6.3 Consumer Electronics

- 6.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.2 Market size and forecast, by region

- 6.3.3 Market share analysis by country

- 6.4 Renewable Energy

- 6.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.2 Market size and forecast, by region

- 6.4.3 Market share analysis by country

- 6.5 Industrial

- 6.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.2 Market size and forecast, by region

- 6.5.3 Market share analysis by country

7: Dry Electrode Technology Market by Region

- 7.1 Overview

- 7.1.1 Market size and forecast By Region

- 7.2 North America

- 7.2.1 Key trends and opportunities

- 7.2.2 Market size and forecast, by Type

- 7.2.3 Market size and forecast, by Application

- 7.2.4 Market size and forecast, by country

- 7.2.4.1 United States

- 7.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.1.2 Market size and forecast, by Type

- 7.2.4.1.3 Market size and forecast, by Application

- 7.2.4.2 Canada

- 7.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.2.2 Market size and forecast, by Type

- 7.2.4.2.3 Market size and forecast, by Application

- 7.2.4.3 Mexico

- 7.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.2.4.3.2 Market size and forecast, by Type

- 7.2.4.3.3 Market size and forecast, by Application

- 7.2.4.1 United States

- 7.3 South America

- 7.3.1 Key trends and opportunities

- 7.3.2 Market size and forecast, by Type

- 7.3.3 Market size and forecast, by Application

- 7.3.4 Market size and forecast, by country

- 7.3.4.1 Brazil

- 7.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.1.2 Market size and forecast, by Type

- 7.3.4.1.3 Market size and forecast, by Application

- 7.3.4.2 Argentina

- 7.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.2.2 Market size and forecast, by Type

- 7.3.4.2.3 Market size and forecast, by Application

- 7.3.4.3 Chile

- 7.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.3.2 Market size and forecast, by Type

- 7.3.4.3.3 Market size and forecast, by Application

- 7.3.4.4 Rest of South America

- 7.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.3.4.4.2 Market size and forecast, by Type

- 7.3.4.4.3 Market size and forecast, by Application

- 7.3.4.1 Brazil

- 7.4 Europe

- 7.4.1 Key trends and opportunities

- 7.4.2 Market size and forecast, by Type

- 7.4.3 Market size and forecast, by Application

- 7.4.4 Market size and forecast, by country

- 7.4.4.1 Germany

- 7.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.1.2 Market size and forecast, by Type

- 7.4.4.1.3 Market size and forecast, by Application

- 7.4.4.2 France

- 7.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.2.2 Market size and forecast, by Type

- 7.4.4.2.3 Market size and forecast, by Application

- 7.4.4.3 Italy

- 7.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.3.2 Market size and forecast, by Type

- 7.4.4.3.3 Market size and forecast, by Application

- 7.4.4.4 United Kingdom

- 7.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.4.2 Market size and forecast, by Type

- 7.4.4.4.3 Market size and forecast, by Application

- 7.4.4.5 Benelux

- 7.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.5.2 Market size and forecast, by Type

- 7.4.4.5.3 Market size and forecast, by Application

- 7.4.4.6 Nordics

- 7.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.6.2 Market size and forecast, by Type

- 7.4.4.6.3 Market size and forecast, by Application

- 7.4.4.7 Rest of Europe

- 7.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.4.4.7.2 Market size and forecast, by Type

- 7.4.4.7.3 Market size and forecast, by Application

- 7.4.4.1 Germany

- 7.5 Asia Pacific

- 7.5.1 Key trends and opportunities

- 7.5.2 Market size and forecast, by Type

- 7.5.3 Market size and forecast, by Application

- 7.5.4 Market size and forecast, by country

- 7.5.4.1 China

- 7.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.1.2 Market size and forecast, by Type

- 7.5.4.1.3 Market size and forecast, by Application

- 7.5.4.2 Japan

- 7.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.2.2 Market size and forecast, by Type

- 7.5.4.2.3 Market size and forecast, by Application

- 7.5.4.3 India

- 7.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.3.2 Market size and forecast, by Type

- 7.5.4.3.3 Market size and forecast, by Application

- 7.5.4.4 South Korea

- 7.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.4.2 Market size and forecast, by Type

- 7.5.4.4.3 Market size and forecast, by Application

- 7.5.4.5 Australia

- 7.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.5.2 Market size and forecast, by Type

- 7.5.4.5.3 Market size and forecast, by Application

- 7.5.4.6 Southeast Asia

- 7.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.6.2 Market size and forecast, by Type

- 7.5.4.6.3 Market size and forecast, by Application

- 7.5.4.7 Rest of Asia-Pacific

- 7.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 7.5.4.7.2 Market size and forecast, by Type

- 7.5.4.7.3 Market size and forecast, by Application

- 7.5.4.1 China

- 7.6 MEA

- 7.6.1 Key trends and opportunities

- 7.6.2 Market size and forecast, by Type

- 7.6.3 Market size and forecast, by Application

- 7.6.4 Market size and forecast, by country

- 7.6.4.1 Middle East

- 7.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.1.2 Market size and forecast, by Type

- 7.6.4.1.3 Market size and forecast, by Application

- 7.6.4.2 Africa

- 7.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 7.6.4.2.2 Market size and forecast, by Type

- 7.6.4.2.3 Market size and forecast, by Application

- 7.6.4.1 Middle East

- 8.1 Overview

- 8.2 Key Winning Strategies

- 8.3 Top 10 Players: Product Mapping

- 8.4 Competitive Analysis Dashboard

- 8.5 Market Competition Heatmap

- 8.6 Leading Player Positions, 2022

9: Company Profiles

- 9.1 AM Batteries

- 9.1.1 Company Overview

- 9.1.2 Key Executives

- 9.1.3 Company snapshot

- 9.1.4 Active Business Divisions

- 9.1.5 Product portfolio

- 9.1.6 Business performance

- 9.1.7 Major Strategic Initiatives and Developments

- 9.2 Maxwell Technologies

- 9.2.1 Company Overview

- 9.2.2 Key Executives

- 9.2.3 Company snapshot

- 9.2.4 Active Business Divisions

- 9.2.5 Product portfolio

- 9.2.6 Business performance

- 9.2.7 Major Strategic Initiatives and Developments

- 9.3 Fraunhofer IWS

- 9.3.1 Company Overview

- 9.3.2 Key Executives

- 9.3.3 Company snapshot

- 9.3.4 Active Business Divisions

- 9.3.5 Product portfolio

- 9.3.6 Business performance

- 9.3.7 Major Strategic Initiatives and Developments

- 9.4 LiCAP Technologies

- 9.4.1 Company Overview

- 9.4.2 Key Executives

- 9.4.3 Company snapshot

- 9.4.4 Active Business Divisions

- 9.4.5 Product portfolio

- 9.4.6 Business performance

- 9.4.7 Major Strategic Initiatives and Developments

- 9.5 Nano Dimension

- 9.5.1 Company Overview

- 9.5.2 Key Executives

- 9.5.3 Company snapshot

- 9.5.4 Active Business Divisions

- 9.5.5 Product portfolio

- 9.5.6 Business performance

- 9.5.7 Major Strategic Initiatives and Developments

- 9.6 Nanotech

- 9.6.1 Company Overview

- 9.6.2 Key Executives

- 9.6.3 Company snapshot

- 9.6.4 Active Business Divisions

- 9.6.5 Product portfolio

- 9.6.6 Business performance

- 9.6.7 Major Strategic Initiatives and Developments

- 9.7 NanoSonic

- 9.7.1 Company Overview

- 9.7.2 Key Executives

- 9.7.3 Company snapshot

- 9.7.4 Active Business Divisions

- 9.7.5 Product portfolio

- 9.7.6 Business performance

- 9.7.7 Major Strategic Initiatives and Developments

- 9.8 NanoSpectra

- 9.8.1 Company Overview

- 9.8.2 Key Executives

- 9.8.3 Company snapshot

- 9.8.4 Active Business Divisions

- 9.8.5 Product portfolio

- 9.8.6 Business performance

- 9.8.7 Major Strategic Initiatives and Developments

- 9.9 Shenzhen Tsingyan Electronic Technology Co.

- 9.9.1 Company Overview

- 9.9.2 Key Executives

- 9.9.3 Company snapshot

- 9.9.4 Active Business Divisions

- 9.9.5 Product portfolio

- 9.9.6 Business performance

- 9.9.7 Major Strategic Initiatives and Developments

- 9.10 Ltd.

- 9.10.1 Company Overview

- 9.10.2 Key Executives

- 9.10.3 Company snapshot

- 9.10.4 Active Business Divisions

- 9.10.5 Product portfolio

- 9.10.6 Business performance

- 9.10.7 Major Strategic Initiatives and Developments

- 9.11 Kionix

- 9.11.1 Company Overview

- 9.11.2 Key Executives

- 9.11.3 Company snapshot

- 9.11.4 Active Business Divisions

- 9.11.5 Product portfolio

- 9.11.6 Business performance

- 9.11.7 Major Strategic Initiatives and Developments

10: Analyst Perspective and Conclusion

- 10.1 Concluding Recommendations and Analysis

- 10.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

By End-User |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the estimated market size of Dry Electrode Technology in 2030?

+

-

What is the growth rate of Dry Electrode Technology Market?

+

-

What are the latest trends influencing the Dry Electrode Technology Market?

+

-

Who are the key players in the Dry Electrode Technology Market?

+

-

How is the Dry Electrode Technology } industry progressing in scaling its end-use implementations?

+

-

What product types are analyzed in the Dry Electrode Technology Market Study?

+

-

What geographic breakdown is available in Global Dry Electrode Technology Market Study?

+

-

Which region holds the second position by market share in the Dry Electrode Technology market?

+

-

How are the key players in the Dry Electrode Technology market targeting growth in the future?

+

-

What are the opportunities for new entrants in the Dry Electrode Technology market?

+

-