Global Disposable Medical Pulp Products Market – Industry Trends and Forecast to 2030

Report ID: MS-855 | Healthcare and Pharma | Last updated: May, 2025 | Formats*:

Disposable Medical Pulp Products The market is the industry dealing with the production and distribution of single-use medical products from processed paper pulp or other natural fibres. Such products are created for use within healthcare facilities for different purposes, such as patient treatment and waste handling. The most important feature of these articles is their disposable nature after they are used only once so that the chances of cross-contamination and hospital-acquired infection are reduced to a minimum. Bedpans, urine bottles, kidney dishes, wash bowls, specimen cups, and most types of procedure trays and waste-handling equipment fall into this category.

The market for disposable medical pulp products is motivated by growing concern for hygiene and infection control in hospitals, clinics, nursing homes, and other healthcare institutions. These products provide an economical and eco-friendly substitute for reusable plastic or metal products, which are usually biodegradable and sometimes recycled products such as newspaper pulp or sugarcane pulp.

Disposable Medical Pulp Products Report Highlights

| Report Metrics | Details |

|---|---|

| Forecast period | 2019-2030 |

| Base Year Of Estimation | 2024 |

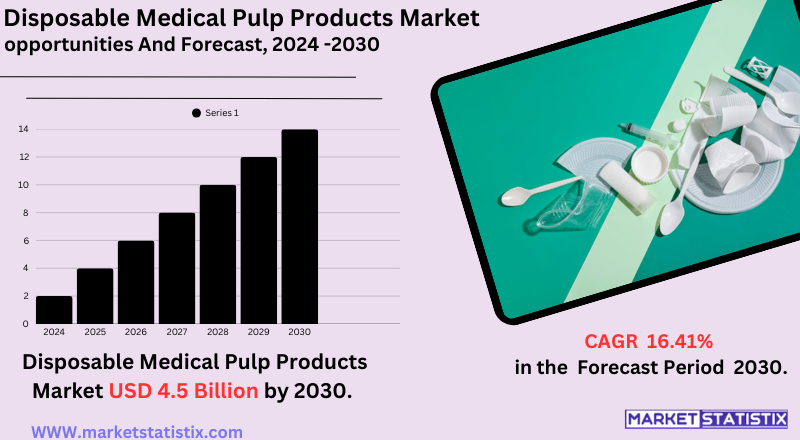

| Growth Rate | CAGR of 16.41% |

| Forecast Value (2030) | USD 4.5 Billion |

| By Product Type | CS Receiver, Detergent Proof Wash Bowl, Kidney Dish, Commode Pan Liner, General Purpose Bowl, Urinals |

| Key Market Players |

|

| By Region |

|

Disposable Medical Pulp Products Market Trends

The market for disposable medical pulp products is already witnessing a few prominent trends. One major influencer is the growing focus on infection control and hygiene in healthcare facilities. The use of these products as one-offs is much preferred for reducing cross-contamination risks and hospital-acquired infections, an issue which has been further highlighted by the recent global healthcare incidents. Therefore, clinics, hospitals, and long-term care facilities are starting to use these disposable solutions in order to provide patient and employee safety.

Another trend with much visibility is the increase in demand for sustainable and environmentally friendly products. As awareness of the environment increases, there is an increased need for medical disposables produced from biodegradable and compostable materials such as sugarcane pulp and recycled paper pulp. This change is also facilitated by tighter environmental controls and waste management regulations that promote the use of sustainable substitutes for plastics. Producers are reacting by developing pulp processing innovations to increase the durability and functionality of these green products, making them a more feasible alternative for a broader array of medical uses.

Disposable Medical Pulp Products Market Leading Players

The key players profiled in the report are Pulpsmith (United Kingdom), Livingstone (Canada), MMS Medical Ltd. (Ireland), Sesneber International (Saudi Arabia), DDC Dolphin Ltd (United Kingdom), Cullen (United States), AMG Medical Inc. (Canada), Caretex (India, Curas Ltd. (Malaysia), Novaleon Pte Ltd. (Singapore), Bosk GmbH (Germany), Vernacare (United Kingdom)Growth Accelerators

The disposable medical pulp products industry is witnessing growth due to numerous driving factors. First, improved awareness and rigid enforcement of infection control in clinical environments are of utmost importance. The use of one-time pulp products greatly lowers the risk of cross-contamination and hospital-acquired infections (HAIs), due to which it is the desired option for achieving hygiene and ensuring patient safety. The spread of infectious diseases increasingly highlights the use of such disposable products in controlling the transmission of pathogens.

Second, the increasing focus on environmental sustainability is a strong driver. Recycled and biodegradable products are commonly produced using medical pulp, providing an environmentally friendly alternative to plastic disposables. The strict environmental regulation and increasing trend towards sustainable healthcare solutions are increasing the uptake of pulp-based products. Also, the rise in the geriatric population and higher prevalence of chronic diseases across the globe are boosting the demand for healthcare services and thus propelling the consumption of disposable medical items utilised during the care of patients and for disposing of wastes.

Disposable Medical Pulp Products Market Segmentation analysis

The Global Disposable Medical Pulp Products is segmented by Type, Application, and Region. By Type, the market is divided into Distributed CS Receiver, Detergent Proof Wash Bowl, Kidney Dish, Commode Pan Liner, General Purpose Bowl, Urinals . The Application segment categorizes the market based on its usage such as Surgeries, Hospitals, Care Facilities. Geographically, the market is assessed across key Regions like North America (United States, Canada, Mexico), South America (Brazil, Argentina, Chile, Rest of South America), Europe (Germany, France, Italy, United Kingdom, Benelux, Nordics, Rest of Europe), Asia Pacific (China, Japan, India, South Korea, Australia, Southeast Asia, Rest of Asia-Pacific), MEA (Middle East, Africa) and others, each presenting distinct growth opportunities and challenges influenced by the regions.Competitive Landscape

The competitive scenario of the market for disposable medical pulp products contains a combination of large, mature companies and some smaller, more specialised firms. Large firms have a wide array of healthcare offerings and enjoy the economies of scale and established sales channels, with which they are able to provide to large hospital systems and large hospitals. Competing among the major players generally revolves around the quality of the product, price, assured supply, and increasingly, how sustainable and green their products are.

Small companies can find niches by focusing on certain types of products or by offering more tailored solutions to specific segments of the healthcare market, for example, nursing homes or speciality clinics. Generally, the competitive landscape is determined by considerations such as the growing need for infection control, the expanding emphasis on sustainable products, and the strict regulatory environment that regulates medical devices and waste management.

Challenges In Disposable Medical Pulp Products Market

The market for disposable medical pulp products has several major challenges that may limit its growth despite growing demand. One of the biggest challenges is the competition from other materials, especially plastics, that are still in broad usage due to their cheaper price and multi-functionality, although they are harmful to the environment. Such price competitiveness affects the customer acceptance of pulp-based products, particularly among cost-sensitive healthcare providers. Secondly, changes in raw material prices and availability – primarily wood pulp – create supply chain risks, which may result in rising costs and shortages of products.

Yet another significant challenge is strict regulatory standards and quality measures varying geographically, raising the cost of compliance and making market entry challenging for producers. Maintaining biocompatibility, uniform product quality, and ensuring medical use safety requires ongoing innovation and stringent testing, which may enhance operating costs. In addition, even though pulp-based medical waste is biodegradable, dumping large amounts of it still involves logistical and environmental issues, even in urban places with poor infrastructure for waste handling. All of these combined therefore pose challenges for the quick adaptation and expansion of disposable medical pulp products in hospitals around the world.

Risks & Prospects in Disposable Medical Pulp Products Market

The transition to more environmentally friendly alternatives to plastics, as well as increased regulation of medical waste disposal, is driving adoption. Product innovation – including the creation of stronger, fully compostable, and antimicrobial pulp products – provides manufacturers an opportunity to differentiate and broaden their offerings. Developing economies, where healthcare infrastructure and waste management capabilities are in the process of emerging, are an untapped source for growth with increasing investment in healthcare and growing demand for infection control.

Geographically, market growth is strong in Europe and North America because of well-developed healthcare systems, stringent regulatory systems, and strong environmental awareness. Yet, Asia-Pacific will be growing at the highest rate, driven by rising healthcare spending, growth in hospital networks, and expanding environmental awareness. Those firms that customise their products to regional healthcare trends and regulations – while adopting automation and eco-friendly manufacturing – are best poised to gain market share worldwide.

Key Target Audience

,

The major target segment in disposable medical pulp product markets are principally hospitals, clinics, nursing facilities, and long-term care establishments needing single-use, sanitary goods for patient use. Such places prefer products such as kidney dishes, urinals, washbowls, and bedpans constructed of biodegradable pulp for their antiseptic effect and single-unit disposal convenience. The procurement function within such venues prioritises respect for health mandates, cost savings, and environmental substitutes over plastic or reusable options.

, Another large audience consists of government health organizations, military medical units, and disaster relief teams that are interested in rapid-deployment, sterile, and sustainable medical products. Suppliers and manufacturers targeting this segment need to factor in the requirements of bulk, uniform supply, regulatory approvals, and increasing demand for environmentally friendly products. Moreover, training and educational institutions for healthcare providers also utilise pulp products for hands-on demonstrations, widening the market base.

Merger and acquisition

Current merger and acquisition (M&A) activity within the disposable medical pulp products market demonstrates a strategic move by dominant players to develop product ranges and build market presence. In March 2021, Vernacare acquired Robinson Healthcare, owner of the UK's number one single-use surgical instrument brand, Instrapac. The move supports Vernacare's buy-and-build strategy, which develops its range of single-use medical products and drives turnover within the group. In the same vein, Bunzl has been aggressively building its healthcare and hygiene portfolio through acquisitions, such as acquiring medical consumables distributors such as Atlas Health Care in Australia and acquiring a majority stake in Nisbets, a UK distributor to the food-service industry, in February 2024.

These strategic purchases are fuelled by increasing demand for biodegradable and environmentally friendly medical products, as healthcare professionals look for sustainable alternatives to conventional plastic disposables. Firms are using M&A to take advantage of this trend, looking to provide end-to-end solutions that comply with strict environmental regulations and infection control requirements. The trend towards consolidation is likely to persist as companies look to improve their capabilities and address the changing needs of the healthcare sector.

>

Analyst Comment

The market for disposable medical pulp products is growing strongly, with the global market worth around USD 3.21 billion in 2024 and expected to grow to USD 5.67 billion by 2033. The growth is fuelled by rising demand for environmentally friendly, single-use medical products in healthcare facilities, as clinics and hospitals focus on infection control, hygiene, and sustainability. The move from conventional plastic-based disposables to biodegradable pulp products is also aided by increased government regulations on medical waste management and worldwide concern for minimising environmental footprints.

- 1.1 Report description

- 1.2 Key market segments

- 1.3 Key benefits to the stakeholders

2: Executive Summary

- 2.1 Disposable Medical Pulp Products- Snapshot

- 2.2 Disposable Medical Pulp Products- Segment Snapshot

- 2.3 Disposable Medical Pulp Products- Competitive Landscape Snapshot

3: Market Overview

- 3.1 Market definition and scope

- 3.2 Key findings

- 3.2.1 Top impacting factors

- 3.2.2 Top investment pockets

- 3.3 Porter’s five forces analysis

- 3.3.1 Low bargaining power of suppliers

- 3.3.2 Low threat of new entrants

- 3.3.3 Low threat of substitutes

- 3.3.4 Low intensity of rivalry

- 3.3.5 Low bargaining power of buyers

- 3.4 Market dynamics

- 3.4.1 Drivers

- 3.4.2 Restraints

- 3.4.3 Opportunities

4: Disposable Medical Pulp Products Market by Type

- 4.1 Overview

- 4.1.1 Market size and forecast

- 4.2 Detergent Proof Wash Bowl

- 4.2.1 Key market trends, factors driving growth, and opportunities

- 4.2.2 Market size and forecast, by region

- 4.2.3 Market share analysis by country

- 4.3 General Purpose Bowl

- 4.3.1 Key market trends, factors driving growth, and opportunities

- 4.3.2 Market size and forecast, by region

- 4.3.3 Market share analysis by country

- 4.4 Kidney Dish

- 4.4.1 Key market trends, factors driving growth, and opportunities

- 4.4.2 Market size and forecast, by region

- 4.4.3 Market share analysis by country

- 4.5 Commode Pan Liner

- 4.5.1 Key market trends, factors driving growth, and opportunities

- 4.5.2 Market size and forecast, by region

- 4.5.3 Market share analysis by country

- 4.6 CS Receiver

- 4.6.1 Key market trends, factors driving growth, and opportunities

- 4.6.2 Market size and forecast, by region

- 4.6.3 Market share analysis by country

- 4.7 Urinals

- 4.7.1 Key market trends, factors driving growth, and opportunities

- 4.7.2 Market size and forecast, by region

- 4.7.3 Market share analysis by country

5: Disposable Medical Pulp Products Market by Application / by End Use

- 5.1 Overview

- 5.1.1 Market size and forecast

- 5.2 Surgeries

- 5.2.1 Key market trends, factors driving growth, and opportunities

- 5.2.2 Market size and forecast, by region

- 5.2.3 Market share analysis by country

- 5.3 Hospitals

- 5.3.1 Key market trends, factors driving growth, and opportunities

- 5.3.2 Market size and forecast, by region

- 5.3.3 Market share analysis by country

- 5.4 Care Facilities

- 5.4.1 Key market trends, factors driving growth, and opportunities

- 5.4.2 Market size and forecast, by region

- 5.4.3 Market share analysis by country

6: Disposable Medical Pulp Products Market by Region

- 6.1 Overview

- 6.1.1 Market size and forecast By Region

- 6.2 North America

- 6.2.1 Key trends and opportunities

- 6.2.2 Market size and forecast, by Type

- 6.2.3 Market size and forecast, by Application

- 6.2.4 Market size and forecast, by country

- 6.2.4.1 United States

- 6.2.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.1.2 Market size and forecast, by Type

- 6.2.4.1.3 Market size and forecast, by Application

- 6.2.4.2 Canada

- 6.2.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.2.2 Market size and forecast, by Type

- 6.2.4.2.3 Market size and forecast, by Application

- 6.2.4.3 Mexico

- 6.2.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.2.4.3.2 Market size and forecast, by Type

- 6.2.4.3.3 Market size and forecast, by Application

- 6.2.4.1 United States

- 6.3 South America

- 6.3.1 Key trends and opportunities

- 6.3.2 Market size and forecast, by Type

- 6.3.3 Market size and forecast, by Application

- 6.3.4 Market size and forecast, by country

- 6.3.4.1 Brazil

- 6.3.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.1.2 Market size and forecast, by Type

- 6.3.4.1.3 Market size and forecast, by Application

- 6.3.4.2 Argentina

- 6.3.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.2.2 Market size and forecast, by Type

- 6.3.4.2.3 Market size and forecast, by Application

- 6.3.4.3 Chile

- 6.3.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.3.2 Market size and forecast, by Type

- 6.3.4.3.3 Market size and forecast, by Application

- 6.3.4.4 Rest of South America

- 6.3.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.3.4.4.2 Market size and forecast, by Type

- 6.3.4.4.3 Market size and forecast, by Application

- 6.3.4.1 Brazil

- 6.4 Europe

- 6.4.1 Key trends and opportunities

- 6.4.2 Market size and forecast, by Type

- 6.4.3 Market size and forecast, by Application

- 6.4.4 Market size and forecast, by country

- 6.4.4.1 Germany

- 6.4.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.1.2 Market size and forecast, by Type

- 6.4.4.1.3 Market size and forecast, by Application

- 6.4.4.2 France

- 6.4.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.2.2 Market size and forecast, by Type

- 6.4.4.2.3 Market size and forecast, by Application

- 6.4.4.3 Italy

- 6.4.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.3.2 Market size and forecast, by Type

- 6.4.4.3.3 Market size and forecast, by Application

- 6.4.4.4 United Kingdom

- 6.4.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.4.2 Market size and forecast, by Type

- 6.4.4.4.3 Market size and forecast, by Application

- 6.4.4.5 Benelux

- 6.4.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.5.2 Market size and forecast, by Type

- 6.4.4.5.3 Market size and forecast, by Application

- 6.4.4.6 Nordics

- 6.4.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.6.2 Market size and forecast, by Type

- 6.4.4.6.3 Market size and forecast, by Application

- 6.4.4.7 Rest of Europe

- 6.4.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.4.4.7.2 Market size and forecast, by Type

- 6.4.4.7.3 Market size and forecast, by Application

- 6.4.4.1 Germany

- 6.5 Asia Pacific

- 6.5.1 Key trends and opportunities

- 6.5.2 Market size and forecast, by Type

- 6.5.3 Market size and forecast, by Application

- 6.5.4 Market size and forecast, by country

- 6.5.4.1 China

- 6.5.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.1.2 Market size and forecast, by Type

- 6.5.4.1.3 Market size and forecast, by Application

- 6.5.4.2 Japan

- 6.5.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.2.2 Market size and forecast, by Type

- 6.5.4.2.3 Market size and forecast, by Application

- 6.5.4.3 India

- 6.5.4.3.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.3.2 Market size and forecast, by Type

- 6.5.4.3.3 Market size and forecast, by Application

- 6.5.4.4 South Korea

- 6.5.4.4.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.4.2 Market size and forecast, by Type

- 6.5.4.4.3 Market size and forecast, by Application

- 6.5.4.5 Australia

- 6.5.4.5.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.5.2 Market size and forecast, by Type

- 6.5.4.5.3 Market size and forecast, by Application

- 6.5.4.6 Southeast Asia

- 6.5.4.6.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.6.2 Market size and forecast, by Type

- 6.5.4.6.3 Market size and forecast, by Application

- 6.5.4.7 Rest of Asia-Pacific

- 6.5.4.7.1 Key market trends, factors driving growth, and opportunities

- 6.5.4.7.2 Market size and forecast, by Type

- 6.5.4.7.3 Market size and forecast, by Application

- 6.5.4.1 China

- 6.6 MEA

- 6.6.1 Key trends and opportunities

- 6.6.2 Market size and forecast, by Type

- 6.6.3 Market size and forecast, by Application

- 6.6.4 Market size and forecast, by country

- 6.6.4.1 Middle East

- 6.6.4.1.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.1.2 Market size and forecast, by Type

- 6.6.4.1.3 Market size and forecast, by Application

- 6.6.4.2 Africa

- 6.6.4.2.1 Key market trends, factors driving growth, and opportunities

- 6.6.4.2.2 Market size and forecast, by Type

- 6.6.4.2.3 Market size and forecast, by Application

- 6.6.4.1 Middle East

- 7.1 Overview

- 7.2 Key Winning Strategies

- 7.3 Top 10 Players: Product Mapping

- 7.4 Competitive Analysis Dashboard

- 7.5 Market Competition Heatmap

- 7.6 Leading Player Positions, 2022

8: Company Profiles

- 8.1 AMG Medical Inc. (Canada)

- 8.1.1 Company Overview

- 8.1.2 Key Executives

- 8.1.3 Company snapshot

- 8.1.4 Active Business Divisions

- 8.1.5 Product portfolio

- 8.1.6 Business performance

- 8.1.7 Major Strategic Initiatives and Developments

- 8.2 Bosk GmbH (Germany)

- 8.2.1 Company Overview

- 8.2.2 Key Executives

- 8.2.3 Company snapshot

- 8.2.4 Active Business Divisions

- 8.2.5 Product portfolio

- 8.2.6 Business performance

- 8.2.7 Major Strategic Initiatives and Developments

- 8.3 Caretex (India

- 8.3.1 Company Overview

- 8.3.2 Key Executives

- 8.3.3 Company snapshot

- 8.3.4 Active Business Divisions

- 8.3.5 Product portfolio

- 8.3.6 Business performance

- 8.3.7 Major Strategic Initiatives and Developments

- 8.4 Cullen (United States)

- 8.4.1 Company Overview

- 8.4.2 Key Executives

- 8.4.3 Company snapshot

- 8.4.4 Active Business Divisions

- 8.4.5 Product portfolio

- 8.4.6 Business performance

- 8.4.7 Major Strategic Initiatives and Developments

- 8.5 Curas Ltd. (Malaysia)

- 8.5.1 Company Overview

- 8.5.2 Key Executives

- 8.5.3 Company snapshot

- 8.5.4 Active Business Divisions

- 8.5.5 Product portfolio

- 8.5.6 Business performance

- 8.5.7 Major Strategic Initiatives and Developments

- 8.6 DDC Dolphin Ltd (United Kingdom)

- 8.6.1 Company Overview

- 8.6.2 Key Executives

- 8.6.3 Company snapshot

- 8.6.4 Active Business Divisions

- 8.6.5 Product portfolio

- 8.6.6 Business performance

- 8.6.7 Major Strategic Initiatives and Developments

- 8.7 Livingstone (Canada)

- 8.7.1 Company Overview

- 8.7.2 Key Executives

- 8.7.3 Company snapshot

- 8.7.4 Active Business Divisions

- 8.7.5 Product portfolio

- 8.7.6 Business performance

- 8.7.7 Major Strategic Initiatives and Developments

- 8.8 MMS Medical Ltd. (Ireland)

- 8.8.1 Company Overview

- 8.8.2 Key Executives

- 8.8.3 Company snapshot

- 8.8.4 Active Business Divisions

- 8.8.5 Product portfolio

- 8.8.6 Business performance

- 8.8.7 Major Strategic Initiatives and Developments

- 8.9 Novaleon Pte Ltd. (Singapore)

- 8.9.1 Company Overview

- 8.9.2 Key Executives

- 8.9.3 Company snapshot

- 8.9.4 Active Business Divisions

- 8.9.5 Product portfolio

- 8.9.6 Business performance

- 8.9.7 Major Strategic Initiatives and Developments

- 8.10 Pulpsmith (United Kingdom)

- 8.10.1 Company Overview

- 8.10.2 Key Executives

- 8.10.3 Company snapshot

- 8.10.4 Active Business Divisions

- 8.10.5 Product portfolio

- 8.10.6 Business performance

- 8.10.7 Major Strategic Initiatives and Developments

- 8.11 Sesneber International (Saudi Arabia)

- 8.11.1 Company Overview

- 8.11.2 Key Executives

- 8.11.3 Company snapshot

- 8.11.4 Active Business Divisions

- 8.11.5 Product portfolio

- 8.11.6 Business performance

- 8.11.7 Major Strategic Initiatives and Developments

- 8.12 Vernacare (United Kingdom)

- 8.12.1 Company Overview

- 8.12.2 Key Executives

- 8.12.3 Company snapshot

- 8.12.4 Active Business Divisions

- 8.12.5 Product portfolio

- 8.12.6 Business performance

- 8.12.7 Major Strategic Initiatives and Developments

9: Analyst Perspective and Conclusion

- 9.1 Concluding Recommendations and Analysis

- 9.2 Strategies for Market Potential

Scope of Report

| Aspects | Details |

|---|---|

By Type |

|

By Application |

|

Report Licenses

Our Team

Frequently Asked Questions (FAQ):

What is the projected market size of Disposable Medical Pulp Products in 2030?

+

-

Which application type is expected to remain the largest segment in the Global Disposable Medical Pulp Products market?

+

-

How big is the Global Disposable Medical Pulp Products market?

+

-

How do regulatory policies impact the Disposable Medical Pulp Products Market?

+

-

What major players in Disposable Medical Pulp Products Market?

+

-

What applications are categorized in the Disposable Medical Pulp Products market study?

+

-

Which product types are examined in the Disposable Medical Pulp Products Market Study?

+

-

Which regions are expected to show the fastest growth in the Disposable Medical Pulp Products market?

+

-

Which application holds the second-highest market share in the Disposable Medical Pulp Products market?

+

-

What are the major growth drivers in the Disposable Medical Pulp Products market?

+

-

The disposable medical pulp products industry is witnessing growth due to numerous driving factors. First, improved awareness and rigid enforcement of infection control in clinical environments are of utmost importance. The use of one-time pulp products greatly lowers the risk of cross-contamination and hospital-acquired infections (HAIs), due to which it is the desired option for achieving hygiene and ensuring patient safety. The spread of infectious diseases increasingly highlights the use of such disposable products in controlling the transmission of pathogens.

Second, the increasing focus on environmental sustainability is a strong driver. Recycled and biodegradable products are commonly produced using medical pulp, providing an environmentally friendly alternative to plastic disposables. The strict environmental regulation and increasing trend towards sustainable healthcare solutions are increasing the uptake of pulp-based products. Also, the rise in the geriatric population and higher prevalence of chronic diseases across the globe are boosting the demand for healthcare services and thus propelling the consumption of disposable medical items utilised during the care of patients and for disposing of wastes.